Few fintech stocks have whipsawed investors like SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) over the past year. After ripping from $10.94 in April 2025 to a 52-week high of $32.73, shares have given back a chunk of those gains.

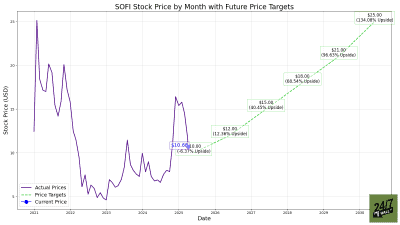

Our 24/7 Wall St. price target for SoFi is $19, implying just 1.26% upside from the current quote. Our recommendation is hold, and our confidence in this base case is high at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $18.76 |

| 24/7 Wall St. Price Target | $19.00 |

| Upside | 1.26% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Round Trip Back to Fair Value

SoFi has traveled a remarkable arc. Shares are up 45.65% over the past year but down 28.34% year to date and 17.76% since the Q4 2025 earnings filing on January 30, 2026.

That sell-off came despite a clean print: adjusted EPS of $0.13 versus $0.11 expected and SoFi’s first-ever billion-dollar quarter at $1.025 billion in revenue. Members hit 13.7 million (+35% YoY), and Q4 loan originations reached a record $10.49 billion. Investors balked at the net interest margin compression of 19 basis points and personal loan charge-offs ticking to 2.80%.

The Case for $25+

Bulls have a credible path. Management is guiding 2026 adjusted revenue to $4.655 billion (~30% growth), adjusted EBITDA to $1.6 billion, and adjusted EPS to $0.60, with a medium-term EPS CAGR of 38% to 42%. The Financial Services segment grew 78% YoY, fee revenue jumped 53%, and the Loan Platform Business is running at a $15 billion annualized pace.

CEO Anthony Noto framed the setup directly: “This combination of scale, innovation, and profitability positions SoFi to drive durable, compounding growth.”

Polymarket traders assign a 91.5% probability SoFi beats the upcoming quarterly print. The Wall Street consensus target sits at $23.48. Our bull case projects $24.91 within 12 months if crypto, stablecoin, and Galileo monetization compound.

The Risks Worth Watching

The bear case starts with valuation. A forward P/E near 49x leaves no margin for error. Net income fell 47.8% YoY in Q4, though that decline reflects a prior-year tax benefit rather than operating performance.

Personal loan charge-offs at 2.80% and Technology Platform accounts down 23% YoY on a single client transition are real concerns, even if the platform headcount loss is largely lapped. With a beta of 2.25, any macro wobble hits SoFi harder than peers. Our bear scenario points to $15.95 over 12 months.

Bottom Line

The franchise is genuinely scaling, but the stock is already pricing in flawless execution. The mid-$15s would mark a level where forward P/E becomes more defensible, while a move above $24 without extended membership and Loan Platform momentum in the Q1 print would test the thesis.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.00 |

| 2027 | $18.41 |

| 2028 | $20.06 |

| 2029 | $20.87 |

| 2030 | $21.84 |

These projections assume SoFi delivers on its 30%+ revenue CAGR through 2028 with gradual multiple compression. Significant upside could emerge if crypto and Galileo scale faster, while a credit cycle break would push prices toward the bear path.