One of the biggest decisions you might have to make for your retirement is figuring out when to claim Social Security.

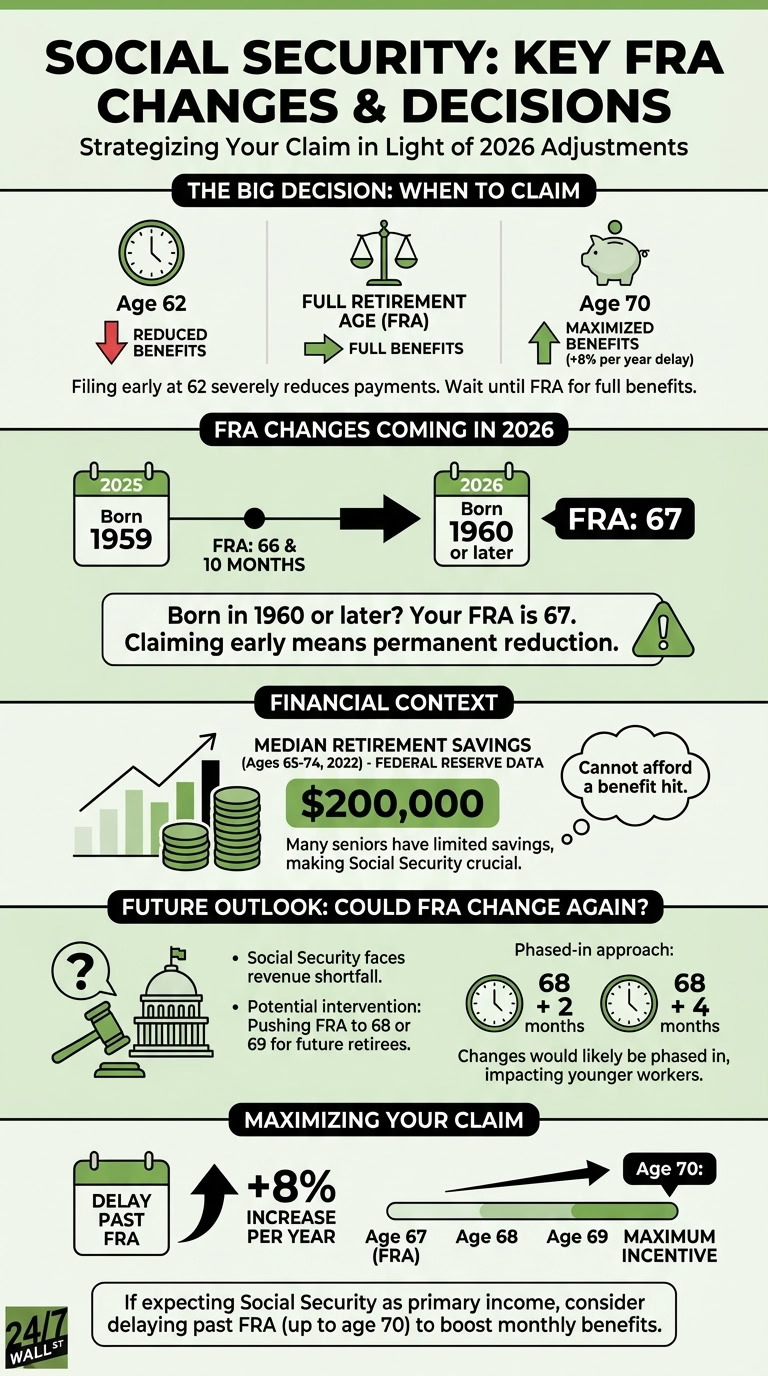

You’re allowed to sign up for benefits at any point as long as you’re at least 62 years old. However, if you file for Social Security at 62, your monthly payments could be severely reduced.

You may, instead, want to wait until full retirement age (FRA) to sign up for Social Security. Once FRA arrives, your Social Security benefits are yours to enjoy without a reduction.

But there’s a big change coming to Social Security’s FRA in 2026 you need to know about. And it may help determine when you sign up to start getting benefits.

How FRA is changing in 2026

It used to be that Social Security’s FRA was 65, which is the same age when Medicare eligibility begins for most enrollees. To conserve funds for Social Security, lawmakers changed the program’s FRA years ago to a range of 66 to 67.

For people with a birth year of 1959 who turn 66 this year, FRA is 66 and 10 months. But for those turning 66 in 2026, FRA is 67.

In fact, anyone born in 1960 or later has an FRA of 67. And it’s important to know that, because claiming Social Security even a month early could result in permanently reduced benefits.

The Federal Reserve puts median retirement savings for seniors ages 65 to 74 at just $200,000 as of 2022. Chances are, that number has increased since then.

But even so, this data tells us that many seniors do not have a lot of money socked away for retirement. People without much savings may not be able to afford a hit to their Social Security benefits.

Could Social Security’s FRA change again?

For now, if you were born in 1960 or later, age 67 is when you’re entitled to your Social Security benefits without a reduction. But that doesn’t mean FRA won’t change again.

Social Security is facing a major revenue shortfall that could result in broad benefit cuts if lawmakers don’t intervene. One change that may help Social Security conserve funds is pushing FRA back by a year or two — for example, making it 68 or 69 for workers born after a certain point of time.

Such a change has been discussed and touted by some lawmakers. And given that Social Security cuts could spur a widespread poverty crisis, it’s a change that may need to be considered.

If lawmakers were to make changes to FRA, they would likely phase it in. Some workers, for example, might see their FRA change to 68 and 2 months, while for others, it could be 68 and 4 months. And if this change happens, it would likely apply to younger workers, as opposed to those on the cusp of retirement.

For now, if you’re nearing retirement, it’s important to know your FRA and wait until at least that point to sign up for Social Security if you expect it to be your primary source of income once you stop working. You should also know that if you delay your Social Security claim past FRA, you can boost your monthly benefits by 8% for every year you do.

This incentive runs out once you turn 70, which is why you shouldn’t delay Social Security beyond that point. But it pays to consider a delayed Social Security claim if you’re nearing retirement without much or any money saved up.