A perception gap is keeping millions of Americans on the sidelines of the stock market. This is especially true if you look at Charles Schwab’s 2025 Modern Wealth Survey, which found that roughly half of non-investors say they do not have enough money to invest, even as brokerage minimums have collapsed and fractional shares let new investors buy in for the price of a coffee. The data on what Americans actually have to work with and what it costs to begin tells a different story from the one most non-investors tell themselves.

The $1,000 Myth

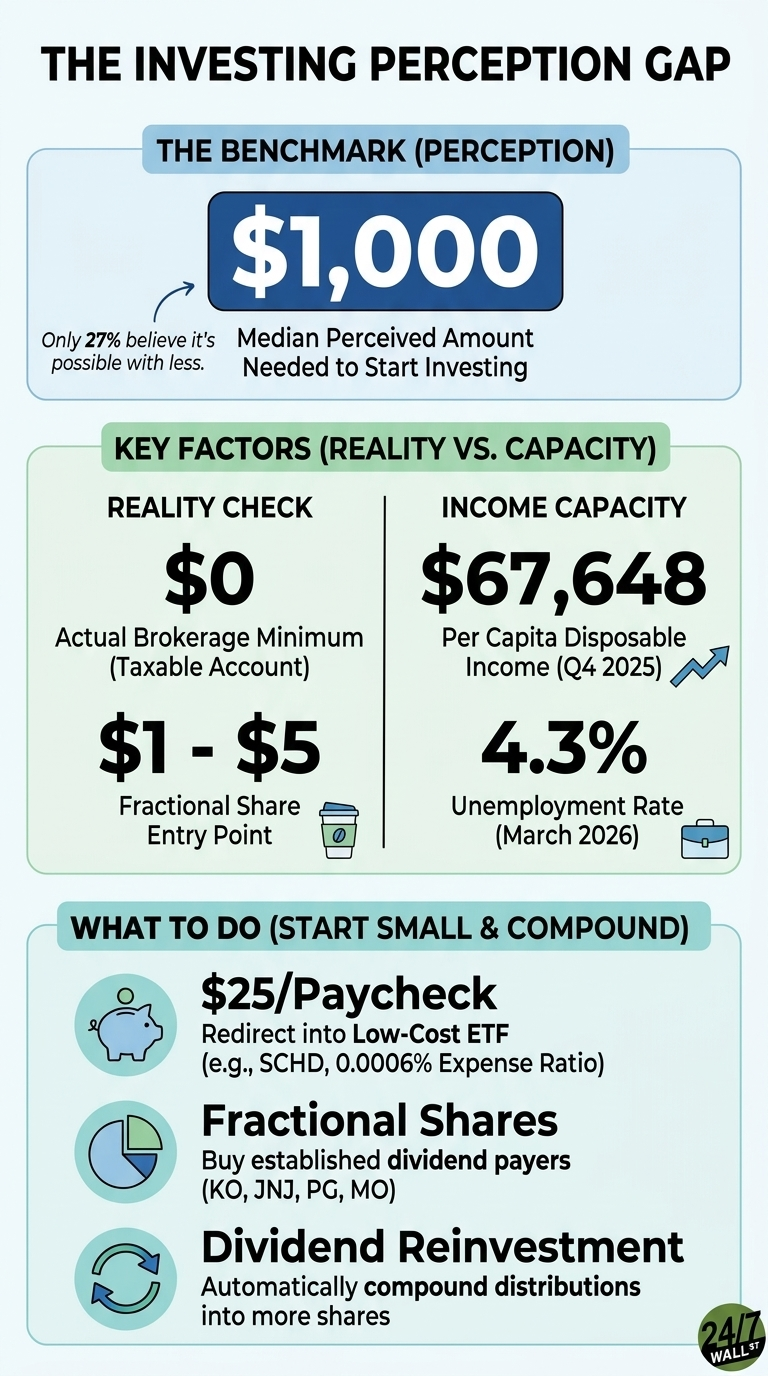

The Schwab survey, conducted April 24 to May 23, 2025, among 2,400 adults ages 21 to 75, asked Americans how much money is needed to start investing. The median answer was $1,000, but only 27% believed it was possible to begin with less than $1,000. That belief is the barrier, not the actual cost of entry.

The reality at most major brokerages is that there is no minimum to open a taxable account, and fractional shares allow purchases as small as $1 or $5 in individual stocks and exchange-traded funds. The Schwab U.S. Dividend Equity ETF (NASDAQ:SCHD | SCHD Price Prediction) trades at $31.31 per share and carries a net expense ratio of 6 basis points. A worker who can redirect $25 a paycheck into a brokerage app can own a slice of a fund that holds roughly $71.6 billion in dividend-paying blue chips.

Income Capacity Americans Already Have

According to federal income data, specifically from the Bureau of Economic Analysis, per capita disposable personal income reached $67,648 in the fourth quarter of 2025, up from $65,247 a year earlier. The personal saving rate was 4%, down from 4.7% in the same quarter of 2024, and the unemployment rate stood at 4.3% in March 2026. Income is rising, and jobs are stable, yet consumer sentiment fell to 53.3 in March 2026, deep in pessimistic territory. Sentiment appears to be the primary driver of the “cannot afford” narrative.

Inflation reinforces the cost of waiting, as the Consumer Price Index reached 330.3 in March 2026, at the 90th percentile of its 12-month range. Cash held outside of an investment account loses purchasing power against that backdrop.

What a Small-Dollar Dividend Foundation Looks Like

For an investor focused on building income rather than chasing growth, established dividend payers offer a starting point. Coca-Cola (NYSE:KO) trades at $78.35 with a 2.66% dividend yield and just raised its quarterly payout to $0.53 per share. Johnson & Johnson (NYSE:JNJ) trades at $227.79, yields 2.29%, and lifted its dividend to $1.34 per share in the most recent declaration. Procter & Gamble (NYSE:PG) at $149.17 just declared a quarterly dividend of $1.0885, the latest in a streak that traces back to 1890.

For a higher current yield, Altria (NYSE:MO) trades at $67.80 with a 6.22% yield and a $1.06 quarterly dividend payable April 30, 2026. All of these stocks can be purchased in fractional amounts at any major retail brokerage offering fractional trading.

Compounding Beats the Headline Number

The case for starting small rests on the dividend growth itself, as Coca-Cola’s quarterly payout has gone from $0.16 in 1999 to $0.53 in 2026. P&G’s quarterly dividend has moved from $0.31 in 2006 to $1.0885 in 2026. SCHD has returned 228.15% over the past 10 years. Delaying contributions until reaching a target balance forgoes the compounding period in between.

How the Mechanics Work Today

- Most major brokerages allow account opening with $0 minimums and support fractional-share purchases starting at $1 or $5.

- Recurring contributions as small as $25 per pay period can be directed to a low-cost dividend ETF, such as SCHD, or a broad index fund.

- Dividend reinvestment options at most brokerages automatically convert each $1.06 Altria distribution or $1.34 Johnson & Johnson payment into additional fractional shares.