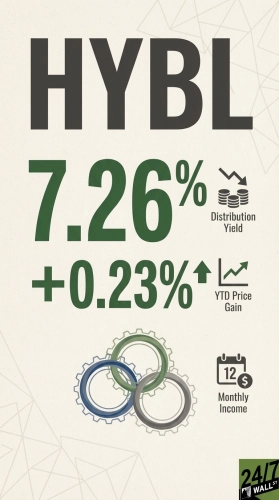

The Janus Henderson AAA CLO ETF (NYSEARCA:JAAA | JAAA Price Prediction) has attracted over $24 billion in assets from income-seeking investors drawn to its 5.3% yield and monthly distributions. For retirees evaluating this fund, understanding how it generates income and whether those payments can continue is essential.

How JAAA Generates Income

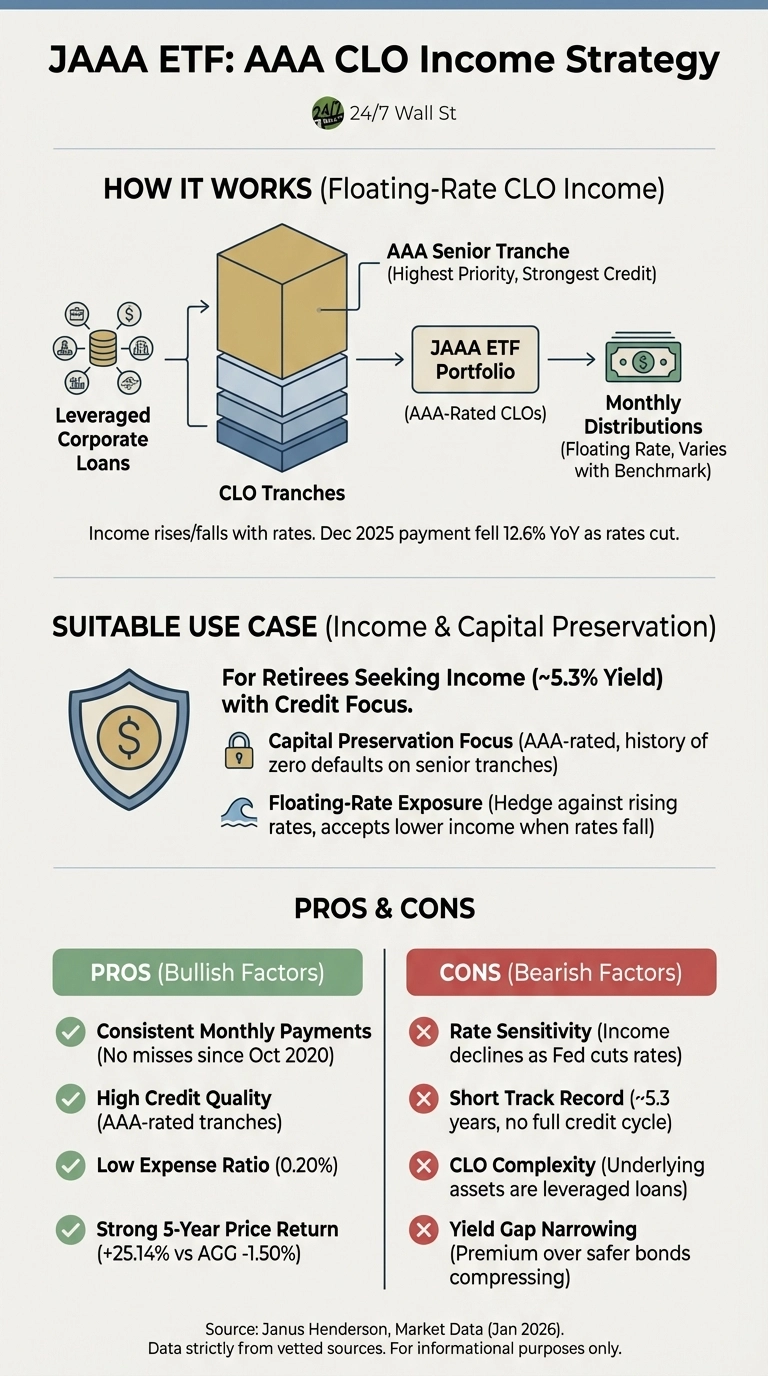

JAAA invests exclusively in AAA-rated tranches of collateralized loan obligations. CLOs are structured securities backed by pools of leveraged loans to corporations. The AAA-rated senior tranches sit at the top of the payment waterfall, receiving interest payments first and enjoying the strongest credit protection. These loans carry floating interest rates tied to benchmark rates, meaning the fund’s income rises and falls with prevailing rates. As borrowers pay interest, that income flows through to JAAA shareholders as monthly distributions.

Dividend Safety: Rate Sensitivity Is the Primary Risk

Since launching in October 2020, JAAA has maintained an unbroken record of 63 consecutive monthly payments. However, the Federal Reserve’s rate-cutting cycle is now putting pressure on distributions. The December 2025 payment fell 12.6% compared to the prior year, reflecting how the fund’s floating-rate structure directly translates lower benchmark rates into reduced income for shareholders.

The credit quality picture remains solid. Moody’s projects U.S. speculative-grade default rates will decline to 3.0% by October 2026, down from 5.3% in October 2025. Since JAAA holds only AAA-rated CLO tranches, the fund benefits from substantial credit insulation even if some underlying borrowers struggle. Historically, these senior tranches have experienced zero defaults.

For retirees, the 5.3% yield tells only part of the story. The fund’s share price has appreciated 5.22% over the past year, combining with distributions to deliver total returns near 10.5%. This positive price performance demonstrates that declining distributions have not eroded principal value.

The fund’s 0.20% expense ratio is exceptionally low for credit exposure, and the $24.3 billion asset base provides ample liquidity. The primary vulnerability is straightforward: if the Fed continues cutting rates through 2026, JAAA’s distributions will likely decline further. Retirees requiring stable, predictable income may find this variability challenging, even though the fund has never missed a payment.

An Alternative Worth Exploring

For investors seeking CLO exposure with broader credit diversification, the VanEck CLO ETF (NYSEARCA:CLOI) offers a different approach. CLOI holds CLO tranches across the credit spectrum rather than limiting itself to AAA-rated securities. This broader approach historically provides higher yields, though the fund currently yields 5.24%—slightly below JAAA’s 5.3%. The tradeoff comes through CLOI’s 0.36% expense ratio, which is higher than JAAA’s rock-bottom 0.20% fee.

CLOI’s diversified credit exposure creates greater sensitivity to default cycles but offers potentially higher income when credit conditions remain stable. Since launching in June 2022, the fund has grown to $1.3 billion in assets, providing a more credit-diversified CLO strategy for investors comfortable accepting additional risk for enhanced return potential.