” I’m 64 with $2.1 million saved, and want to retire but don’t know if it’s possible.” Every week, we hear from readers in nearly this exact position.

They’ve done the hard part right: saved diligently, built a seven-figure portfolio, and arrived at their mid-60s with real financial flexibility. The question is no longer “Can I retire?” — it’s whether their withdrawal strategy, tax planning, and portfolio construction can realistically support 25 to 30 years of spending in the face of market volatility, rising healthcare costs, and shifting tax rules.

While $2.1m looks strong on the surface, the long-term outcome depends on a handful of strategic decisions that matter far more than headline net worth alone.

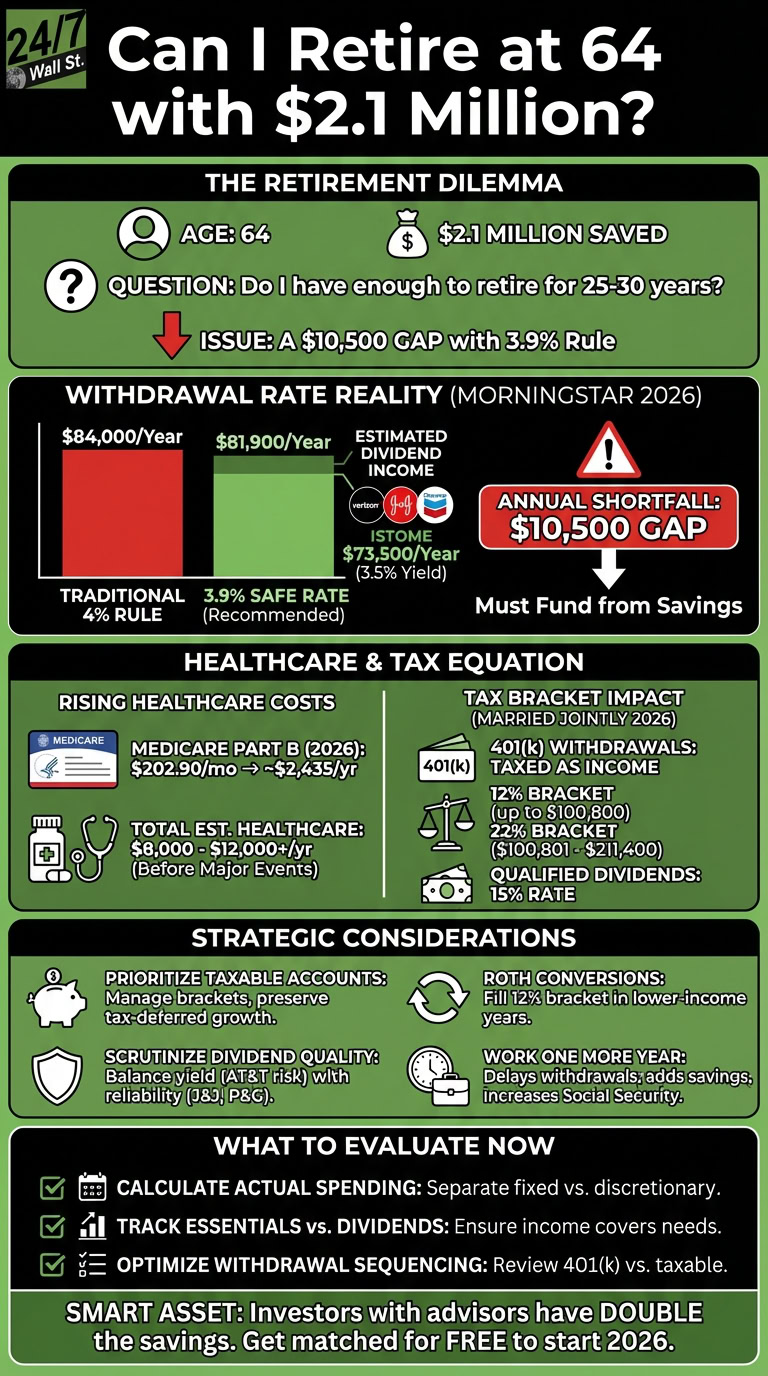

| Age: | 64 years |

| Savings: | $2.1 million |

| Question: | “Do I have enough to retire?” |

| Issue: | A $10,500 gap that appears, following Morningstar’s 3.9% withdrawal rules |

The Withdrawal Rate Reality

The traditional 4% rule suggests withdrawing $84,000 annually from $2.1 million. However, Morningstar’s 2026 research recommends a more conservative 3.9% starting rate ($81,900), reflecting current market valuations and sequence-of-returns risk that hits hardest in the first five years. Retiring into a market downturn and selling shares to fund withdrawals locks in losses that compound over decades.

Your portfolio appears income-focused with positions in dividend payers like Verizon (6.77% yield), Johnson & Johnson (2.49% yield), and Chevron (4.13% yield). At an estimated blended yield of 3.5%, you could generate roughly $73,500 in annual dividend income without selling shares. That leaves a $10,500 gap if following the 3.9% guideline, requiring strategic withdrawals from your 401(k) or taxable accounts.

New data shows that investors who work with a financial advisor have DOUBLE the savings as those who don’t

And Smart Asset is making it easier than ever to get started, and is matching investors with advisors serving their arrea for FREE to start 2026 There is nothing to lose. Investors are matched after answering a few questions, and it takes 5 minutes or less.

The Tax and Healthcare Equation

Turning 65 in 2026 brings Medicare eligibility, but costs are rising. The standard Medicare Part B premium is $202.90 monthly in 2026, up from $185 in 2025, totaling nearly $2,435 annually. Add Part D prescription coverage, supplemental insurance, and out-of-pocket expenses, and healthcare could easily consume $8,000-$12,000 per year before major medical events.

The tax picture depends on account structure. If most of your $2.1 million sits in a traditional 401(k), every withdrawal is taxed as ordinary income. For married couples filing jointly in 2026, the 12% bracket extends to $100,800 of taxable income, while the 22% bracket covers income up to $211,400. Withdrawing $82,000 from a 401(k), combined with Social Security benefits starting in a few years, could push you into the 22% bracket. Qualified dividends in taxable accounts receive preferential 15% rates for most retirees.

Strategic Considerations That Matter

The split between 401(k) and taxable accounts creates opportunity. Prioritize spending from taxable accounts first to manage your tax bracket, especially before required minimum distributions begin at age 73. This preserves tax-deferred growth while utilizing lower capital gains rates. Consider partial Roth conversions during lower-income years before Social Security begins, filling up the 12% bracket without triggering higher rates.

Your dividend portfolio needs scrutiny. AT&T cut its dividend 47% in 2022, a reminder that high yields sometimes signal distress. UnitedHealth, despite strong cash flow, has faced regulatory concerns that have impacted its stock performance. Quality dividend aristocrats like Johnson & Johnson and Procter & Gamble offer lower yields but greater reliability and growth. Balance income needs with the reality that a 20-30 year retirement requires portfolio growth to outpace inflation.

Working one additional year dramatically improves sustainability. It delays portfolio withdrawals, allows another year of contributions, postpones Social Security (increasing monthly benefits by roughly 8% annually until age 70), and reduces the years your portfolio must fund.

What to Evaluate Now

Calculate your actual annual spending needs rather than relying on withdrawal rate guidelines. Track fixed costs like housing, healthcare, and insurance separately from discretionary spending you can adjust during market downturns. Assess whether your dividend income covers essential expenses, creating a buffer against selling during corrections. Review your 401(k) versus taxable account balance to optimize withdrawal sequencing.