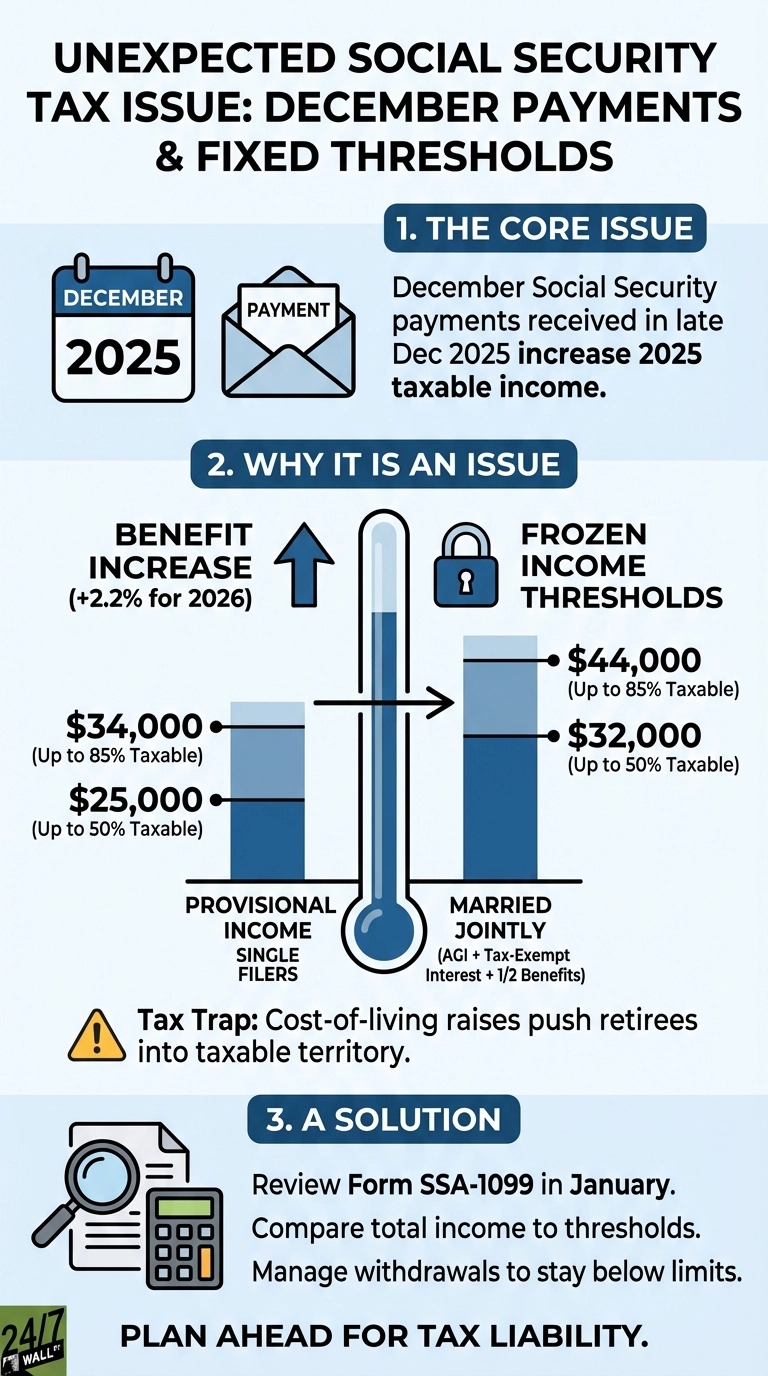

If you received Social Security payments in December 2025, you may face an unexpected tax surprise when filing your 2025 return. The timing of when benefits arrive determines which tax year they count toward, and December payments can push retirees over income thresholds that trigger taxation of benefits.

Why December Payments Create Tax Complications

Social Security operates on an unusual payment schedule: benefits are paid the month after they’re earned. Your January 2026 payment represents your December 2025 benefit. Most retirees receive 12 months of Social Security income during calendar year 2025, with payments arriving between January 2025 and January 2026.

Social Security benefits are taxed based on when you receive them, not when they’re earned. If you received a payment in early January 2026, that money counts toward your 2026 tax return. However, beneficiaries who received payments in late December 2025 saw those amounts increase their 2025 taxable income.

The Provisional Income Threshold That Catches Retirees

The IRS uses “provisional income” to determine Social Security taxation—a calculation that adds your adjusted gross income, tax-exempt interest, and half your benefits. Single filers face their first tax hurdle at $25,000 in provisional income, where up to half of benefits become taxable. The structure creates a cliff effect where a small income increase can suddenly trigger taxation on thousands of dollars in benefits.

Married couples filing jointly get slightly more breathing room with a $32,000 threshold, but the same cliff effect applies. The challenge intensifies at higher income levels, where 85% of benefits face taxation once single filers exceed $34,000 or married couples cross $44,000.

That extra December payment becomes problematic when combined with other 2025 income. Treasury bonds currently yielding over 4% generate taxable interest, and required minimum distributions from retirement accounts add to the total. Together, these income sources can push retirees who normally stay below the thresholds into taxable territory for 2025.

Planning Around Payment Timing

Congress set these income thresholds decades ago and never adjusted them for inflation. While your benefits increased 2.2% this year to keep pace with rising costs, the taxation thresholds remained frozen. This creates a trap where cost-of-living adjustments designed to protect purchasing power instead push more retirees into taxable territory.

Review your Form SSA-1099, which arrives in January and reports your total Social Security income for the prior year. Compare that figure to your other income sources. If you’re close to a threshold, consider strategies like managing retirement account withdrawals or timing the sale of investments to stay below the limits.

Everyone’s situation differs based on their specific benefit amount, other income sources, and filing status. The goal is understanding how payment timing interacts with annual income calculations, helping you anticipate your tax liability rather than discovering it at filing time.