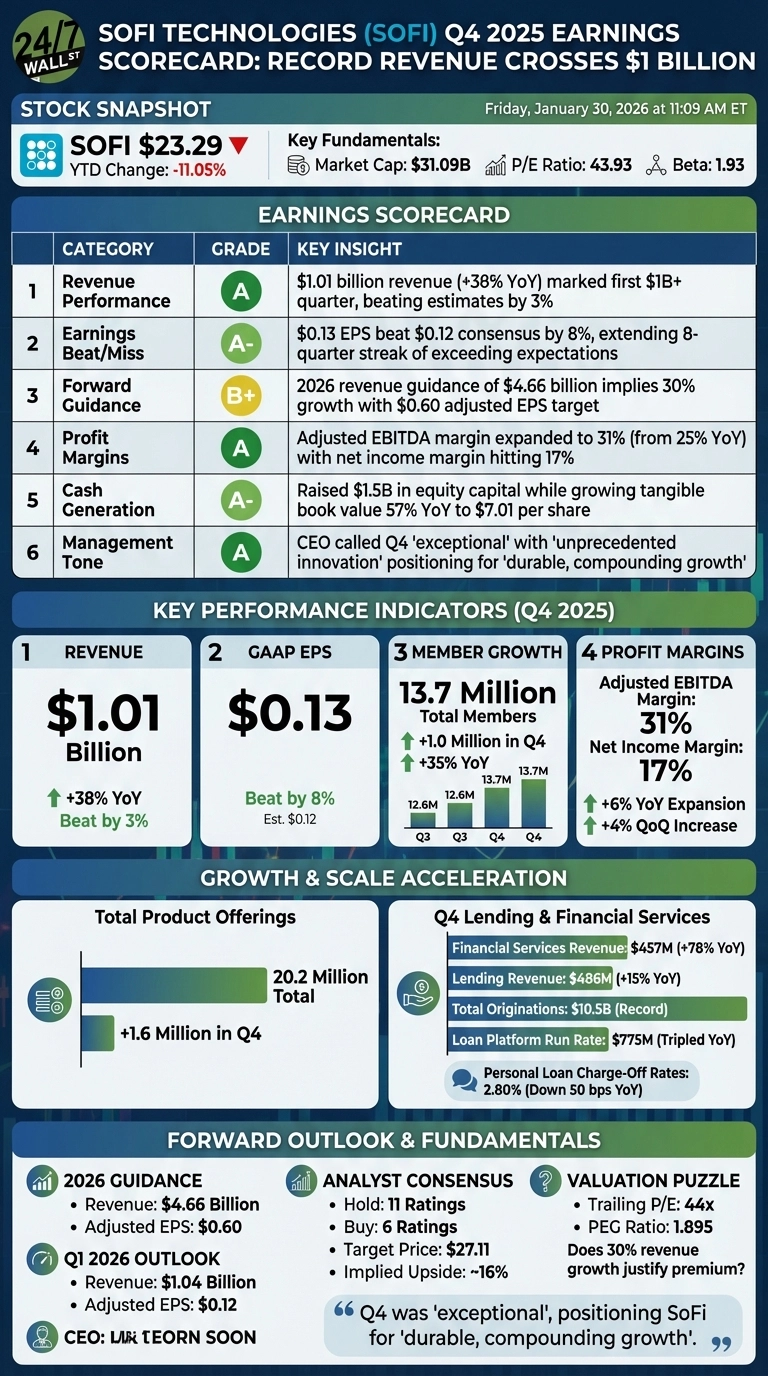

SoFi Technologies (Nasdaq: SOFI | SOFI Price Prediction) crossed the $1 billion quarterly revenue threshold for the first time in company history, delivering Q4 2025 results that beat estimates across the board while adding a record 1 million new members. The fintech platform reported revenue of $1.01 billion versus the $982 million consensus, alongside GAAP EPS of $0.13 that surpassed the $0.12 estimate by 8%.

Despite the strong quarterly performance, investors digested the company’s aggressive $1.5 billion capital raise in December and parsed through 2026 guidance expectations and the stock is down 6.10% at mid-day.

Earnings Scorecard

Record Member Growth Drives Platform Scale

SoFi added 1 million members in Q4 alone, the first time the company achieved seven-figure quarterly member growth, bringing total members to 13.7 million (up 35% YoY). The platform now supports 20 million product relationships after adding a record 1.6 million products in the quarter, pushing the cross-buy rate to 40%.

Financial Services revenue surged 78% YoY to $457 million with 51% contribution margins, while the Lending segment generated $486 million (up 15%) on record $10.5 billion in total originations. Personal loan charge-off rates improved to 2.80% annualized, down 50 basis points YoY, demonstrating strong credit quality among borrowers with average FICO scores of 746.

The company’s loan platform business, which transfers loans to partners, reached a $775 million annualized run rate after transferring $3.7 billion in Q4, tripling YoY.

Bottom Line: Strong Fundamentals, Valuation Questions

SoFi delivered an unambiguous operational win with record metrics across member growth, revenue scale, and profitability expansion. The 31% EBITDA margin and 17% net income margin demonstrate the platform’s improving unit economics as it scales.

However, the stock’s decline and analyst consensus of 11 Hold ratings (versus 6 Buy ratings) suggest the market has priced in much of this growth. Trading at 44x trailing earnings with a $27.11 average price target implying 16% upside, investors face a valuation puzzle: does 30% revenue growth justify the premium multiple?

The Q1 2026 guidance calling for $1.04 billion revenue and $0.12 adjusted EPS (doubling Q1 2025) will be the immediate test of whether SoFi can sustain momentum after this milestone quarter.