SoFi Technologies (NASDAQ: SOFI | SOFI Price Prediction) reported Q1 2026 results before the open on April 29, 2026, beating on revenue and meeting on EPS. Investors did not reward the earnings report. Shares are down 13% in morning trading today, despite the fastest adjusted net revenue growth in three years. The market wanted a guide-up. It did not get one.

Lending Engine Hits a New Gear

The growth story is hard to argue with. Reported revenue came in at $1.10 billion versus a $1.05 billion consensus, with adjusted net revenue tracking roughly 41% growth. Lending revenue jumped 55% to $642.4 million on record originations of $12.18 billion, up 68% year over year. Financial Services revenue rose 41%, and net interest income climbed 39% to $693 million.

Members grew 35% to 14.7 million, products were up 39%, and 43% of new products came from existing members. I liked the cross-buy data. It is the cleanest signal that the bundle is working.

Guidance Stays Put, Bulls Get Cold Feet

Management reaffirmed full-year adjusted net revenue near $4.655 billion, adjusted EBITDA around $1.6 billion, and adjusted EPS of about $0.60, but did not raise. After four straight quarters of double-digit beats, a clean “meet” on EPS plus an unchanged outlook was enough to flip the script. Technology Platform also got worse, with revenue down 27% on a large client departure and enabled accounts off 16%. Credit metrics ticked up too: personal loan charge-offs rose to 3.03% from 2.80% sequentially.

The Quarter in Figures

- Adjusted EPS: $0.12, in line with consensus

- Revenue: $1.10B vs. $1.05B expected, beat of ~4.9%

- GAAP Net Income: $166.7M, up 134.45% YoY

- Adjusted EBITDA: $339.9M at a 31% margin

- Deposits: $40.24B, with cost of funds down 48 basis points YoY

- Day-of Stock Reaction: -13%

The unchanged guide is the line to focus on. That is the line that turned a strong quarter into a sell.

Noto Sticks to the Compounding Pitch

CEO Anthony Noto said SoFi “had an excellent Q1 delivering another quarter of durable growth and strong returns, fueled by our relentless focus on innovation and brand building.” He also flagged the “strategic entry into new areas like digital assets”, including the SoFiUSD stablecoin and a Mastercard settlement tie-in. The tone was confident, not promotional.

What I’m Watching Into Q2

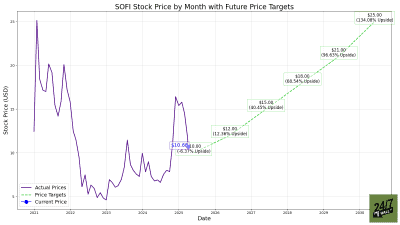

Two things matter from here. First, whether Technology Platform stabilizes after the client loss. Second, whether credit holds up as charge-offs creep higher. If management raises the FY guide on the next earnings report, today’s reaction looks like an overreaction worth revisiting. If not, the $23.48 average analyst target gets harder to defend.