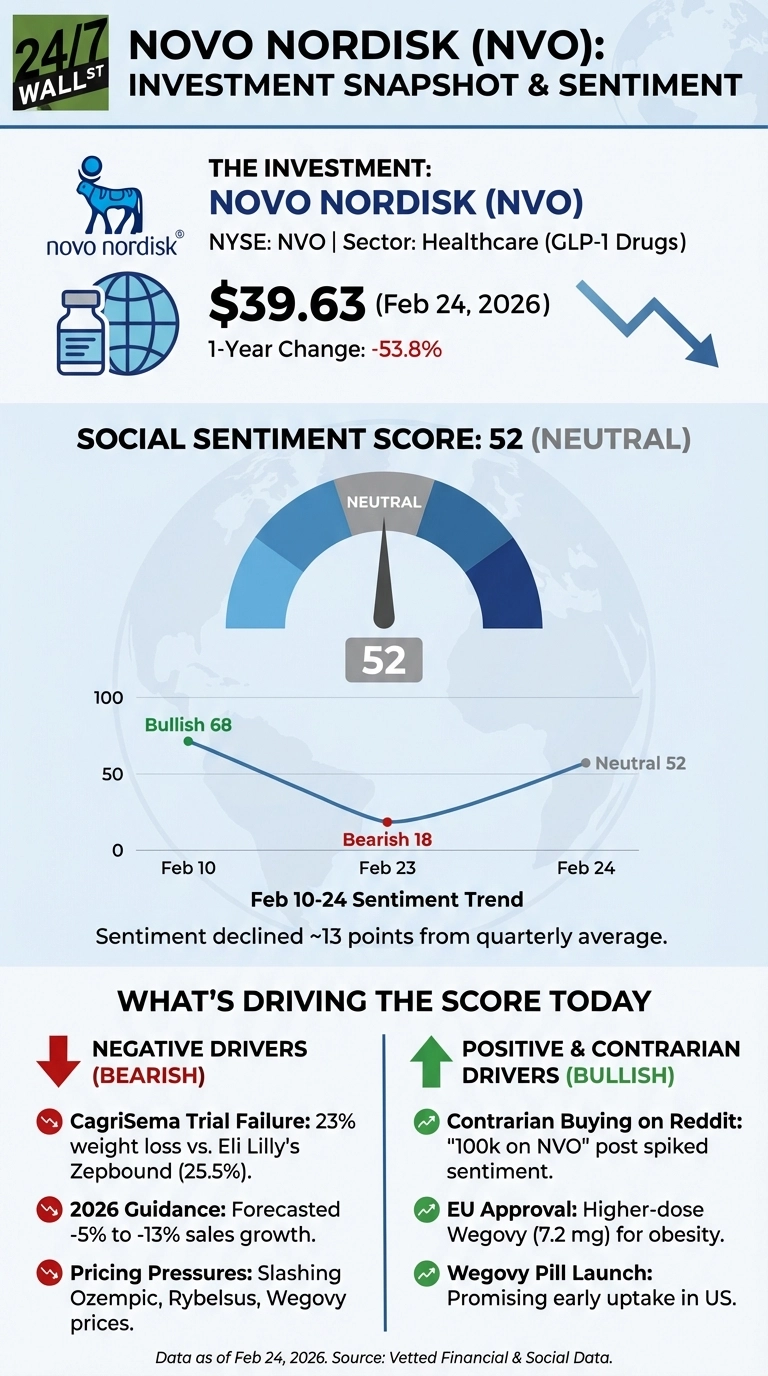

After finding itself some unwanted attention this week, Novo Nordisk (NYSE:NVO | NVO Price Prediction) has dropped 22% in the past week and 56% over the past year, now sitting near its 52-week low. As a result, Reddit sentiment has followed along with this downward shift, sliding from a quarterly average of 56 to a weekly average of 43 after two damaging stories hit in rapid succession: a clinical trial failure and a plan to cut prices on flagship drugs.

CagriSema’s Miss Hands Eli Lilly a Wider Lead

On February 23, REDEFINE-4 trial results showed CagriSema produced 23% average body weight loss versus 25.5% for Eli Lilly (NYSE:LLY) Zepbound, a sizable blow for Novo’s efforts in this space. The most immediate result of this reveal was that JPMorgan downgraded Novo from Overweight to Neutral, slashed CagriSema forecasts by 40-63% for 2027-2030, and cut group sales estimates by 2-16% through 2030. Additionally, Deutsche Bank and Kepler Cheuvreux lowered their ratings, and the company’s 12-month average price target now sits at $54.25, with three analysts at Sell or Strong Sell and only two at Buy-equivalent, suggesting professional conviction has clearly shifted.

The pricing news arrived the same week Novo announced it will slash list prices for Ozempic, Rybelsus, and Wegovy to $675/month effective January 1, 2027, down from Wegovy’s current price of roughly $1,349/month. A Navitus Health Solutions survey found 7 in 10 GLP-1 users say cost influenced their treatment decisions, so the move addresses a real barrier, but it also validates the pricing pressure Novo already flagged in its 2026 guidance of -5% to -13% sales growth.

Reddit Is Split: Panic Sellers vs. Contrarian Buyers

The r/stocks community drove the most analytical discussion, with the post “Novo Nordisk sinks 10% after weight loss drug fails to match Eli Lilly’s in trial” accumulating 762 upvotes and 146 comments.

Novo Nordisk sinks 10% after weight loss drug fails to match Eli Lilly’s in trial

by r/stocks

“The 2.5% gap vs Zepbound might sound small but in a competitive market where payers and patients have a choice, that margin matters enormously for formulary placement. This isn’t just a trial miss – it’s a commercial positioning problem.” – u/equities_nerd42

r/wallstreetbets took the opposite view. The post “I see fat people everywhere – 100k on NVO” gathered 336 upvotes and 125 comments, with sentiment spiking to 82 (very bullish) by early Tuesday, a sharp reversal from the 18 (very bearish) reading when trial results first broke.

I see fat people everywhere – 100k on NVO

by r/wallstreetbets

“Obesity isn’t going away. NVO still has Wegovy, the pill formulation just launched, and the stock is down 50%+ from its highs. I’m not selling – I’m loading. 100k in, let’s ride.” – u/fat_stacks_NVO (reflecting one retail investor’s personal position, not a recommendation)

Genuine Offsets, But the Thesis Has Changed

The EU recently approved a 7.2 mg higher-dose Wegovy on February 17, showing 20.7% average weight loss versus 17.5% for the standard dose, although a U.S. FDA decision is still pending. Early Wegovy pill scripts reached roughly 48,000 in Week 7, up 12% week-over-week, which has helped the stock trade at 13x trailing earnings. Analysts are debating whether the current valuation reflects a durable repricing of the company’s competitive position or a temporary overreaction to the trial results. The answer depends on whether CagriSema’s pipeline value and the oral Wegovy launch can offset the formulary share Novo is likely to cede to Lilly in 2026 and 2027. The Annual General Meeting will take place on March 26, where new board members will be voted on, which could signal whether management is prepared to defend its pipeline strategy or pivot.