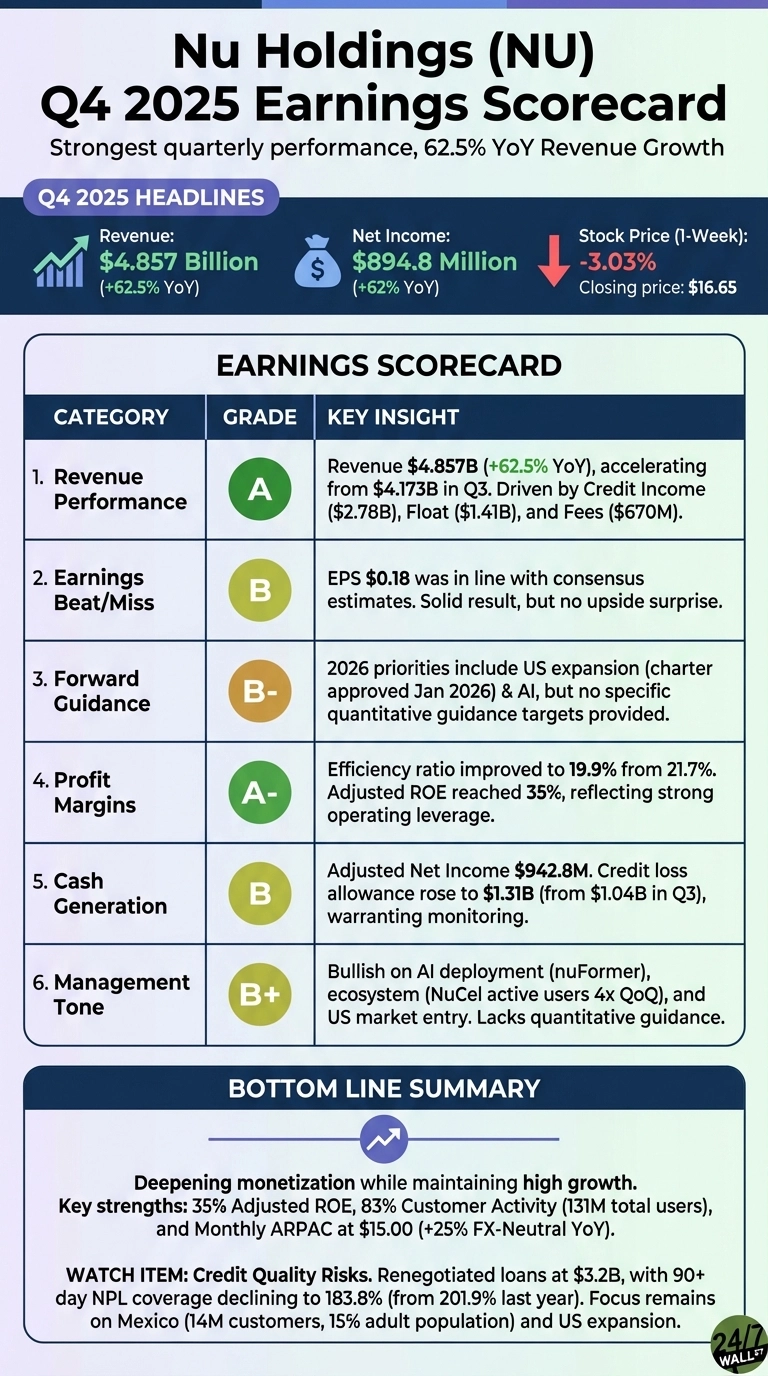

Nu Holdings closed out 2025 with its strongest quarterly performance yet, posting $4.857 billion in Q4 revenue, up 62.5% year-over-year, while net income surged 62% to $894.8 million. Despite the impressive numbers, shares slipped 3.03% over the week following the report, closing at $16.65, suggesting investors had priced in much of the growth already. For a company now serving 131 million customers across Latin America, the question is whether the next leg of growth can sustain this trajectory.

Q4 2025 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | A | Revenue of $4.857B grew 62.5% YoY, accelerating from $4.173B in Q3 2025, driven by credit income of $2.78B, float income of $1.41B, and fee income of $670M. |

| Earnings Beat/Miss | B | EPS of $0.18 came in exactly in line with consensus estimates, a solid result but leaving no upside surprise to reward shareholders. |

| Forward Guidance | B- | Management outlined three strategic priorities for 2026, including US expansion after receiving conditional national bank charter approval in January 2026, but provided no specific revenue or EPS targets, limiting near-term visibility. |

| Profit Margins | A- | The efficiency ratio improved to 19.9% from 21.7% in Q4 2024, and adjusted ROE reached 35%, reflecting strong operating leverage at scale. |

| Cash Generation | B | Adjusted net income of $942.8M reflects healthy earnings quality, though the credit loss allowance rose to $1.31B from $1.04B in Q3, a meaningful build that warrants monitoring. |

| Management Tone | B+ | Commentary was bullish across AI deployment via nuFormer, ecosystem expansion with NuCel growing 4x QoQ in active users, and US market entry, though the absence of quantitative guidance tempers the grade. |

Bottom Line

Nu’s Q4 results demonstrate a company still in high-growth mode while simultaneously improving profitability. The combination of a 35% adjusted ROE, an 83% customer activity rate across 131 million users, and a 25% FX-neutral rise in monthly revenue per active customer to $15.00 paints a picture of deepening monetization. The main watch item heading into 2026 is credit quality: renegotiated loans stand at $3.2B and the 90+ day NPL coverage ratio has declined to 183.8% from 201.9% a year ago. With the Mexico banking license pending and US expansion in early stages, execution risk is real. Investors should watch whether Mexico customer growth, currently at 14 million or 15% of the adult population, can accelerate once full banking capabilities are unlocked.