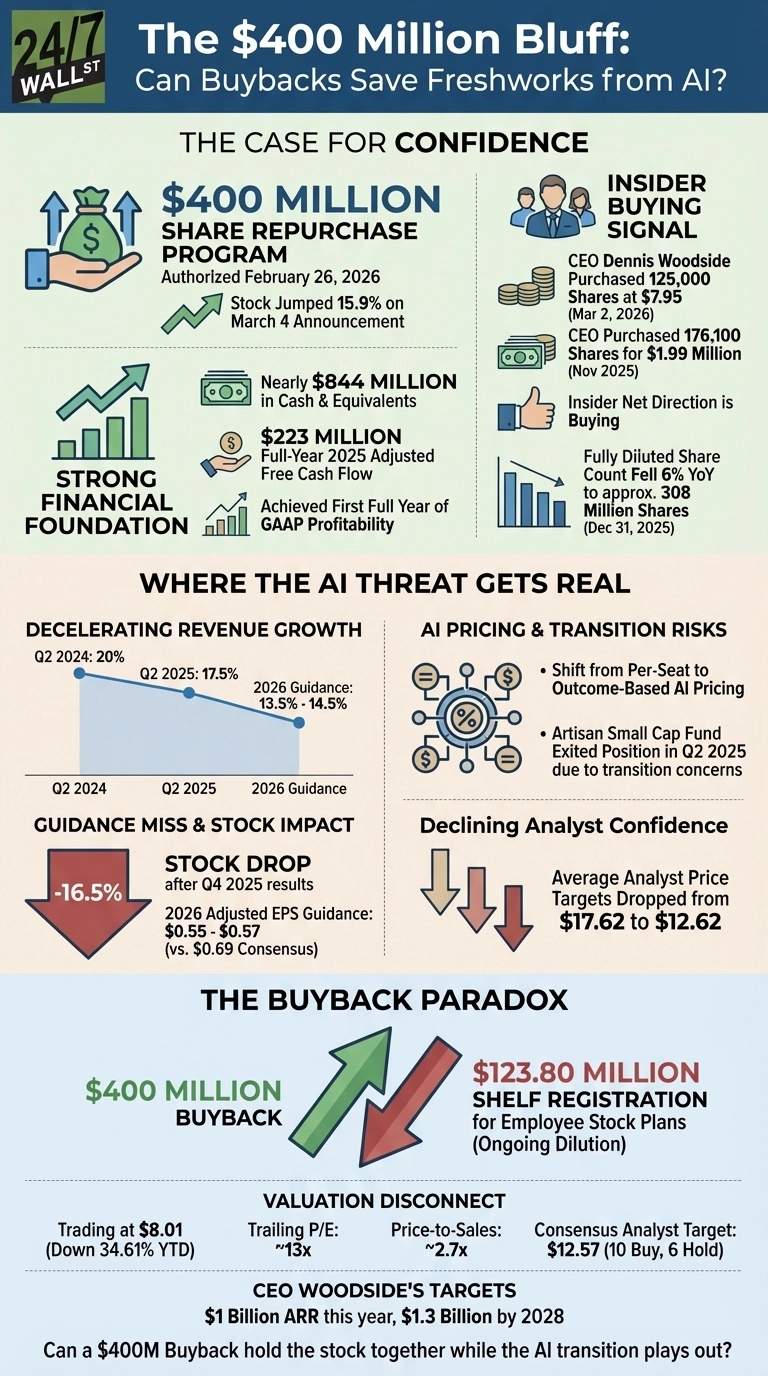

Helping over 74,000 businesses like Sony and Bridgestone, Freshworks, which provides AI-powered, cloud-based software (NASDAQ:FRSH | FRSH Price Prediction) is trading at $8.01, down 34.61% year-to-date and 47.37% over the past year. Against that backdrop, management just authorized a $400 million share repurchase program on February 26, 2026. The stock jumped 15.9% on March 4 following the announcement, then gave most of it back, and it’s this whipsaw that captures the central tension investors face right now.

The Case for Confidence

The buyback is not a stretch, as Freshworks closed 2025 with nearly $844 million in cash, equivalents, marketable securities, and restricted cash and generated $223 million in full-year 2025 adjusted free cash flow, while achieving its first full year of GAAP profitability.

In addition to company performance, CEO Dennis Woodside has been buying alongside shareholders: he purchased 125,000 shares at $7.95 on March 2, 2026, and 176,100 shares for $1.99 million in November 2025. The insider net direction is buying, as the fully diluted share count fell 6% year over year to approximately 308 million shares as of December 31, 2025, showing the program is already doing real work.

Where the AI Threat Gets Real

The harder question is what the business looks like in three years, as revenue growth has decelerated from 20% in Q2 2024 to 17.5% in Q2 2025, with full-year 2026 guidance of 13.5% to 14.5% growth. When Q4 2025 results hit in February, the 2026 adjusted EPS guidance of $0.55 to $0.57 came in significantly below the consensus of $0.69, sending the stock down 16.5%. Average analyst price targets dropped from $17.62 to $12.62 in the following weeks.

The structural risk is the shift from per-seat pricing to outcome-based pricing for AI. Artisan Small Cap Fund exited its position in Q2 2025, citing “concerns about the company’s ability to transition effectively from a seat-based to an enterprise-based pricing model, particularly in light of AI’s impact on customer performance and employee levels.”

Woodside frames it differently: “We’re not the incumbent that has a lot to lose. We’re the attacker who’s taking the share.” Freddy AI ARR reached $25 million by Q4 2025, nearly doubling year over year, with a three-year target of $100 million in AI-driven ARR. Customers paying for AI SKUs show 116% net dollar retention, compared with the overall base rate of 108%.

The Buyback Paradox

At $8.01, Freshworks trades at a trailing P/E of roughly 13x and a price-to-sales ratio of about 2.7x against trailing revenue of $838.8 million. The consensus analyst target sits at $12.57, implying meaningful upside, with 10 buy ratings and 6 holds. But those same analysts just cut their targets, and a concurrent $123.80 million shelf registration for employee stock plans introduces ongoing dilution that the buyback must work against.

Woodside’s 2026 target is clear: “Freshworks’ 2025 results bring me confidence in our march towards $1 billion in annual recurring revenue this year and $1.3 billion by 2028.” Whether a $400 million buyback can hold the stock together while the AI transition plays out is the question investors will be watching through every quarterly report this year.

Data Sources:

- Citizens and Oppenheimer analyst price target cuts (February 11, 2026): used for analyst reaction context and Freddy AI ARR milestone confirmation [Source: Citizens and Oppenheimer Cut Freshworks Inc. (FRSH) Price Targets After Q4 Results]

- Freshworks executive insider sale analysis: used for Mika Yamamoto Rule 10b5-1 sale context and retained ownership details [Source: A Freshworks Executive Sold Over 32,000 Company Shares. Is the Stock a Buy or Sell?]