Packaged-food giants have spent 2026 dodging two big headwinds: GLP-1 drugs that shrink appetites for snacks and store brands that steal share on price. Organic sales across the sector have turned negative for the second straight year. Yet Kraft Heinz (NASDAQ:KHC | KHC Price Prediction) just hit pause on the very breakup Wall Street once cheered.

New CEO Steve Cahillane, who came on in January specifically to split the company, shelved those plans after six weeks. Instead, he told 35,000 employees to focus on fixing the core business and using its scale as an edge. For retail investors hunting income and a turnaround, the move raises a simple question: buy now or keep waiting?

Why a Change in Course?

Cahillane arrived with a track record — he led Kellogg’s 2023 split and sold the snacks business to Mars for $36 billion. Kraft Heinz itself announced breakup plans last fall to separate fast-growing sauces and condiments from slower grocery staples. But Cahillane quickly concluded the business wasn’t strong enough for a clean split.

“Do we separate and then have potentially two companies that are not as strong as we would like them to be? Or do we fix the business, and then we have options to separate in the future?” he recently told The New York Times.

The decision lines up with Warren Buffett’s view. Buffett, whose Berkshire Hathaway helped engineer the 2015 Kraft-Heinz merger and remains the largest shareholder, publicly called the breakup idea “disappointing” back in September. Cahillane didn’t call Buffett directly, but updated Berkshire CEO Greg Abel on the pivot. In short, the new boss chose repair over rupture.

The Numbers Don’t Lie

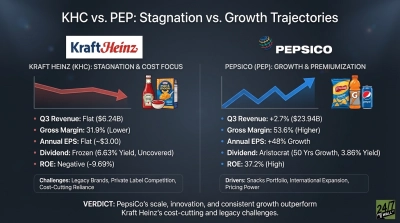

Let’s look at the latest data from Kraft Heinz’s fourth-quarter and full-year 2025 earnings release. Full-year net sales hit $24.9 billion, down 3.5% from the prior year; organic sales fell 3.4%. Volume and mix dropped 4.1 percentage points, while price added just 0.7 points. Sales have now declined for nine straight quarters.

Yet cash generation tells a different story. Net cash from operations reached $4.5 billion, up 6.6%. Free cash flow climbed to $3.7 billion, up 15.9%, helped by lower capital spending and better working capital. At a recent share price of $22.49 and market cap of $26.6 billion, that works out to a free-cash-flow yield of roughly 14%. The company also pays a $1.60 per share annual dividend for a yield of 7.1%.

Granted, GAAP net income swung to a $5.85 billion loss for the year — largely from one-time items that produced trailing-12-month losses of $4.93 per share. Adjusted operating results, however, still generated positive earnings power. Cahillane announced a $600 million investment in “commercial levers” to drive profitable growth and paused all breakup work.

How Kraft Heinz Stacks Up

Compare Kraft to peer General Mills (NYSE:GIS), another staple-food name facing similar volume pressure. It trades at a forward P/E around 11.7 times versus Kraft’s roughly 10.5 times on adjusted earnings. General Mills’ dividend yield sits at 6.5% compared to 7.1% for Kraft. General Mills’ free cash flow yield is also less than its rival’s, 8.5% to 14%. Both companies also saw organic sales slide in their latest reports, but Kraft Heinz’s cash machine runs hotter.

No matter how you slice it, Kraft Heinz trades at a discount to peers on cash flow, while offering a fatter payout. The stock sits near one of its lowest levels since the 2015 merger, yet the balance sheet has improved, and the new CEO is plowing money into innovation instead of financial engineering.

Key Takeaway

Kraft Heinz is a buy today if you seek high current income and believe management can stabilize volumes. The 7.1% dividend yield and 14% free cash flow yield provide a cushion, while Cahillane reinvests in brands and R&D for GLP-1-era consumers.

Risks remain, of course: Sales have fallen for more than two years, and consumer shifts won’t reverse overnight — but the breakup is off the table, and cash flow is rising. Smart investors who bought at these depressed levels have locked in both yield and potential upside as the fix takes hold. In short, the numbers now support ownership more than they did six months ago.