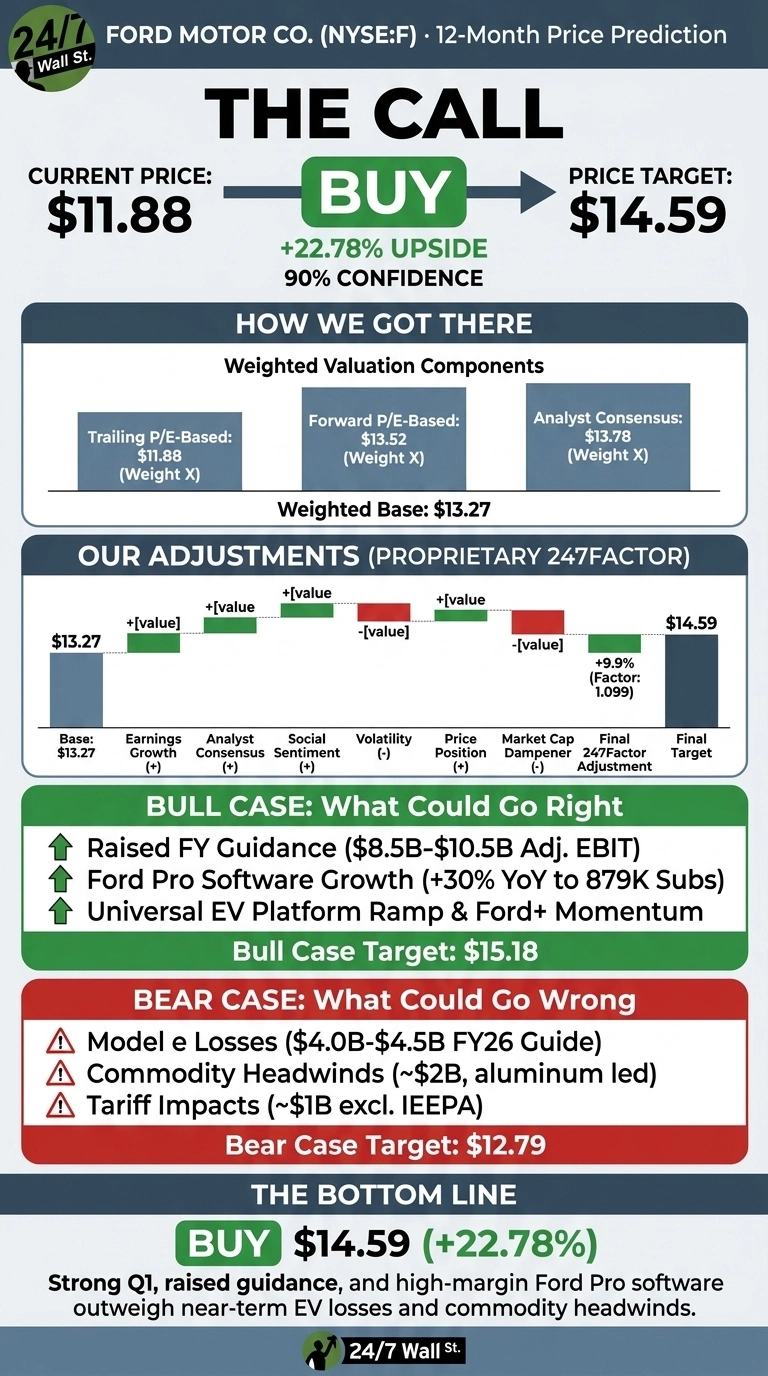

Our 24/7 Wall St. price target for Ford (NYSE:F | F Price Prediction) is $14.59 over the next 12 months, implying 22.78% upside from the current price of $11.88. Our recommendation is buy, with a confidence level of 90%. Ford’s raised full-year guidance, expanding Ford Pro software base, and deeply discounted forward multiple form the foundation of our call.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $11.88 |

| 24/7 Wall St. Price Target | $14.59 |

| Upside | 22.78% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Choppy Year Built on a Strong Q1

Ford has gained 22.6% over the past year, but year-to-date the stock is down 8.49% and slipped 4.04% in the past week. The 52-week range runs from $9.53 to $14.80, leaving F roughly 7% off the high.

Q1 2026, reported April 29, 2026, was the catalyst. EPS came in at $0.66 on revenue of $43.25 billion (+6% YoY), with adjusted EBIT of $3.49 billion. Management raised full-year adjusted EBIT guidance to $8.5 billion to $10.5 billion and free cash flow to $5 billion to $6 billion.

RBC Capital Markets raised its price target from $11 to $13, keeping a sector perform rating. A separate 179,000-vehicle Bronco and Ranger seat recall tempered enthusiasm into early May.

Why Bulls See a Breakout to $15+

The bull case rests on Ford Pro and Ford Blue. Ford Blue posted $23.9 billion of revenue in Q1 (+14%) on F-Series, Bronco, Explorer, and Expedition demand. Ford Pro generated 11.4% margins, and paid software subscriptions grew 30% YoY to 879,000, a high-quality recurring stream.

CEO Jim Farley stated: “Our strong first-quarter results and raised full-year guidance reflect the momentum of the Ford+ plan.” If commodity costs ease and the Universal EV platform launches on time, our bull-case scenario points to $15.18 within 12 months. A 4.97% dividend yield pays investors to wait.

The Risks Worth Watching

Bears point to the Model e segment, which lost $777 million in Q1 and is guided to $4 billion to $4.5 billion of full-year losses. Commodity headwinds of $2.0 billion (led by aluminum) and tariff impacts of $1 billion compress 2026 earnings, and the Q1 result included a non-recurring $1.30 billion IEEPA tariff benefit.

Wholesale units fell 4% YoY. Bulls argue the Model e drag reflects deliberate investment in the Universal EV platform that should narrow losses in 2027 and beyond. Our bear-case scenario lands at $12.79.

Why I’d Buy Ford Here

Our 24/7 Wall St. price target of $14.59 and buy rating reflect a stock trading at a forward P/E of 8 with a 4.97% dividend, raised guidance, and a high-margin software business in Ford Pro. Confidence is 90%.

I’d be a buyer if commodity pressure peaks in the second half and Ford Pro margins hold above 11%. I’d stay on the sidelines if Model e losses blow past the $4.5 billion ceiling or if the SAAR slips below the 16.0 million floor.

Ford Price Prediction 2026-2030

Looking ahead, here is where our model projects Ford could trade in the coming years, assuming current growth trajectories and a gradual recovery in EV economics.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $14.59 |

| 2027 | $16.50 |

| 2028 | $18.50 |

| 2029 | $20.25 |

| 2030 | $21.96 |

These projections assume Ford executes on the Ford+ plan and Universal EV ramp. Significant upside or downside could result from EV adoption pace, tariff policy shifts, or a U.S. recession.