Jim Cramer’s well-documented skepticism on Microsoft (NASDAQ:MSFT | MSFT Price Prediction) traces back to the company’s January earnings, when a strong headline beat triggered one of the worst single-day reactions the stock has seen in years. The question for investors now is whether the skepticism still holds after another quarter of results.

The Quarter That Sparked the Skepticism

On Jan. 28, Microsoft posted Q2 FY2026 EPS of $4.14 against a $3.8486 estimate, a 8% beat on revenue of $81.27 billion. The market response was brutal: a -10% day-of decline, then -9% over the next week. Our team covered the disconnect here.

The culprit was capital intensity. CapEx surged 89% year-over-year to $29.88 billion, while Azure growth came in at 39%. Investors began asking the obvious question: where is the return on the spend?

What the Pattern Shows

Across the last five quarters, Microsoft has beaten EPS five out of five times, yet the average one-week reaction is -4%. Even Q1 FY2026’s 13% EPS surprise produced a -3% day-of move. This is the structural concern Cramer has zeroed in on: expectations are running ahead of what beats can satisfy.

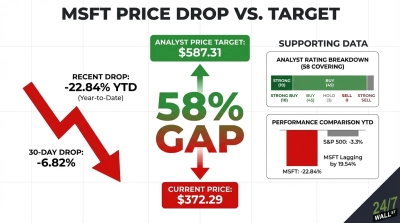

The damage shows up on the chart. MSFT is down 14% year-to-date and 14% from the January earnings close, trading near $410.20 as of May 5.

The Counter-Case From Q3 FY2026

The April quarter, reported April 29, gave bulls something to work with. Revenue hit $81.3 billion, Azure demand “continues to exceed available supply,” and Microsoft 365 Copilot seat additions rose over 160% year-over-year to 15 million paid seats. The AI business hit a $37 billion annualized run rate, up 123%. CFO Amy Hood directly addressed the CapEx critique: “If we had allocated the GPUs that just came online in Q1 and Q2 entirely to Azure, the KPI would have been over 40.” Filing details are available via the SEC 8-K.

Is the Skepticism Justified?

Cramer’s call is partly vindicated by price action. Five straight beats and the stock still trades at a forward multiple of 30x earnings while sliding. Polymarket pricing gives just a 0.195 probability that MSFT closes above $420 by May 8. The bull thesis is intact on fundamentals; the bear thesis is about valuation digesting an $625 billion RPO and a CapEx cycle that needs to monetize. Both can be true at once, and that is the tension Cramer is pointing at.