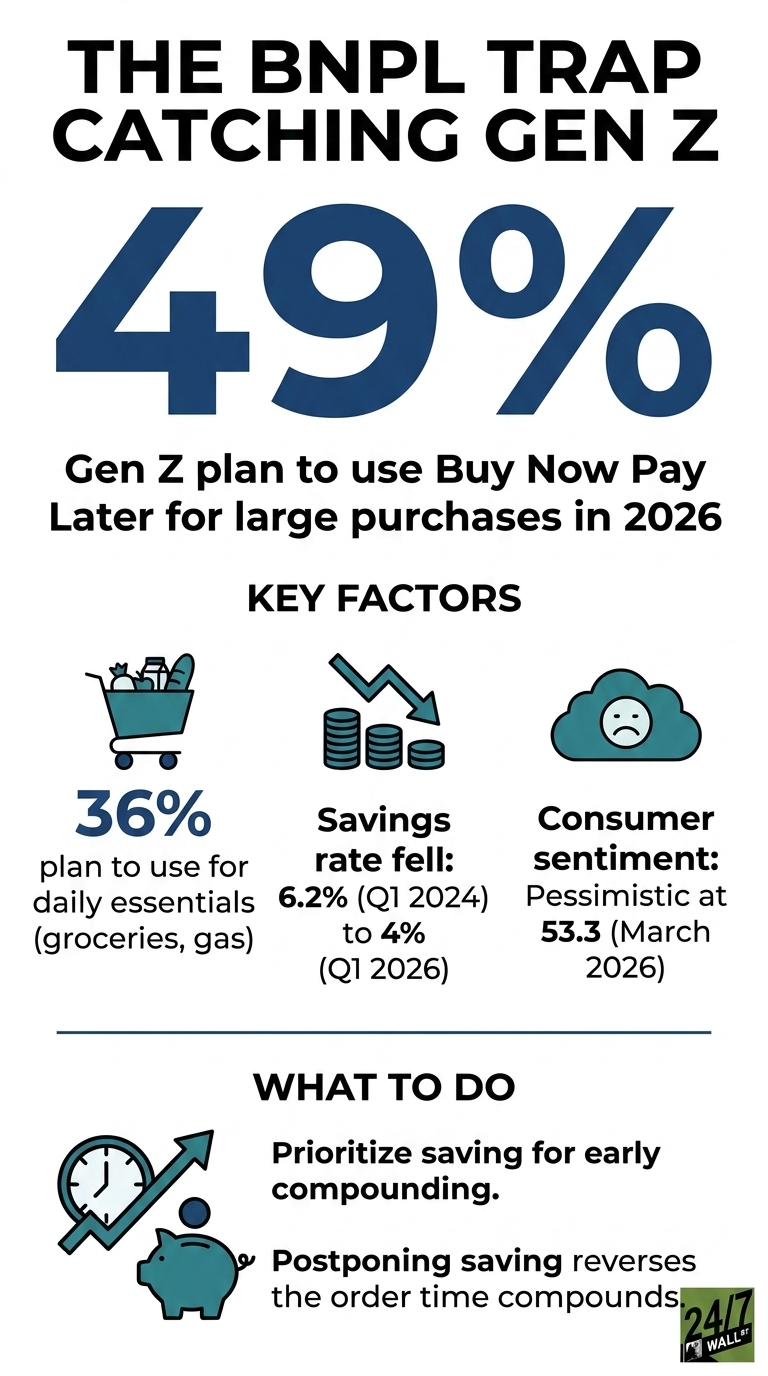

Buy Now Pay Later services have moved from a checkout novelty to a core part of how Gen Z pays for things, including items people used to pay for with cash or a debit card. The latest 2026 P&P Wave I Data Deck: The Financial States of America from Northwestern Mutual finds that 49% of Gen Z plan to use Buy Now Pay Later for large purchases in 2026, and 36% plan to use it for daily essentials like groceries and gas. Those two numbers describe a generation financing its life in installments before most members have built meaningful savings.

Consumer prices have continued to rise, and that steady climb has weighed on people’s feelings about their financial lives. Measures of consumer sentiment remain subdued even as the labor market holds relatively steady with unemployment in the low-to-mid 4% range. At the same time, the personal savings rate has declined over the past two years even as disposable income has continued to grow, reflecting households’ willingness to keep consuming despite thinner financial cushions. When spending rises while savings fall, installment-based financing tends to spread more quickly, and the current environment fits that pattern.

Essentials on Installment

The 36% figure for daily essentials is the one worth sitting with. Splitting a couch into four payments is one thing. Splitting a grocery run is something else entirely. When food and housing costs keep climbing faster than wages, deferring the grocery bill by a few weeks starts to feel less like a red flag and more like a reasonable workaround. That is the part that is easy to miss in the headline number. It is not just a spending habit. It is a sign that a generation is quietly normalizing installment debt for purchases that most people never used to think twice about paying upfront. And once that normalization takes hold, it tends to show up elsewhere on the balance sheet too.

BNPL Sits On Top Of An Already Crowded Debt Stack

These households carry other balances in addition to BNPL. The same report finds that credit cards remain the top source of personal debt by a wide margin, more than double car loans and roughly four times medical debt. Among Americans who carry personal debt, the average balance is $21,700, and 65% of U.S. adults carry some form of personal debt outside of a mortgage. BNPL plans layer on top of that stack, often without showing up on a traditional credit report, making total exposure harder for the borrower to track.

The behavioral pattern follows in the same dataset. 62% of U.S. adults with debt prioritize paying it down, compared to 38% who prioritize saving. For a 22-year-old, that ratio matters more than for a 55-year-old, because dollars not invested in early years are the ones that would have compounded longest. A Gen Z worker funneling cash into four-payment plans for groceries in 2026 is postponing the start of the compounding clock.

What The Cycle Costs Decades Out

The 49% and 36% figures describe a checkout habit, but the long tail is a retirement question. Gen Z has the longest investment horizon of any working generation, which lengthens the compounding window for early contributions to a 401(k), IRA, or brokerage account. Routing discretionary income into installment payments, then into credit card minimums, and only then into savings reverses the order in which time compounds. The savings rate data already show households consuming a larger share of their disposable income, and the BNPL figures suggest that this pattern is concentrated among the cohort that can least afford to lose early compounding years.

The data documents what is happening. A meaningful share of Gen Z is entering adulthood, paying for ordinary purchases on a delayed basis while inflation runs hot, sentiment runs low, and the national savings rate compresses. Whether that becomes a temporary coping mechanism or a structural feature of the generation’s balance sheet remains the open question behind the 49% headline.