Emerging markets climbed over 25% in 2025 while trading at deep discounts to U.S. equities. That combination of momentum and relative value creates an unusual setup for 2026 that retirees seeking diversification should consider.

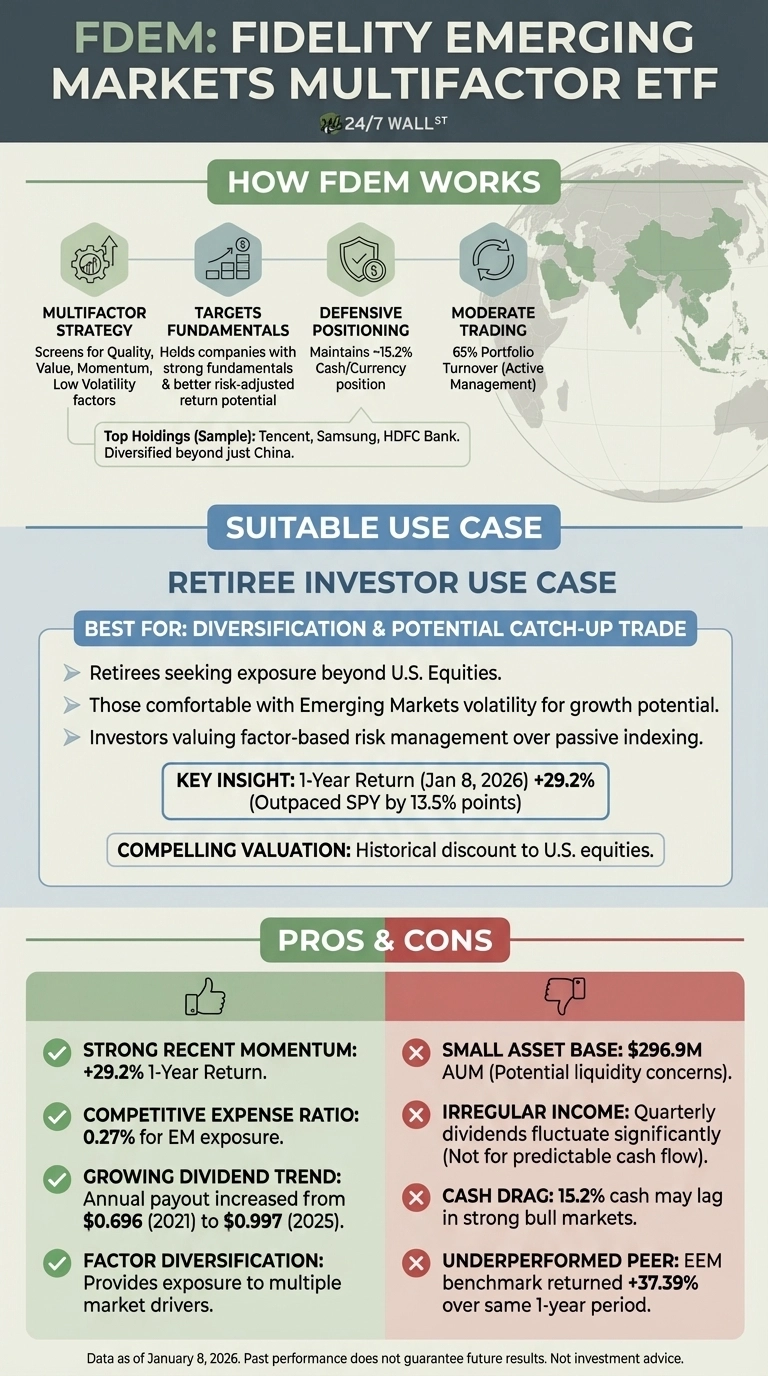

The Fidelity Emerging Markets Multifactor ETF (NYSEARCA:FDEM) screens for quality, value, momentum, and low volatility factors across developing economies. The fund holds $296.9 million in assets and delivered a 29.2% one-year return through early January 2026, outpacing the SPDR S&P 500 ETF Trust (NYSEARCA:SPY | SPY Price Prediction) by over 13 percentage points.

What Multifactor Means for Portfolio Construction

FDEM doesn’t track a market-cap-weighted index. It tilts toward companies scoring well on multiple investment factors, holding Tencent (OTC:TCEHY), Samsung Electronics (OTC:SSNLF), and HDFC Bank (NYSE:HDB) among top positions while maintaining a 15% cash position.

This factor-based approach targets companies with stronger fundamentals and better risk-adjusted returns than pure index strategies. For retirees, that means potentially smoother performance during volatile periods, though 65% portfolio turnover means more frequent trading than passive alternatives.

The Valuation Case Remains Compelling

Emerging markets have historically traded at discounts to U.S. equities, a pattern that persisted even after 2025’s strong performance. Earnings growth expectations for emerging markets have improved heading into 2026, with projections showing strength relative to non-U.S. developed markets.

The fund’s 0.27% expense ratio is competitive for an actively managed factor strategy. It pays a 1.85% dividend yield with quarterly distributions that grew from $0.696 in 2021 to $0.997 in 2025, though individual payments fluctuate significantly.

Tradeoffs Worth Understanding

The fund’s small asset base creates potential liquidity concerns during market stress. With under $300 million in assets, FDEM could face wider bid-ask spreads or difficulty executing large trades compared to category giants. The high cash position, while defensive, means missing gains when emerging markets rally hard.

Factor strategies can underperform when momentum or value falls out of favor. Retirees must accept FDEM may lag simpler index approaches in certain environments, and the irregular dividend schedule doesn’t suit those needing predictable quarterly income.

Who Should Look Elsewhere

Retirees needing consistent, predictable income should avoid FDEM. Quarterly dividends vary substantially, making cash flow planning difficult. Those with limited emerging markets knowledge or low risk tolerance should reconsider, as developing economies bring currency risk, political instability, and higher volatility than domestic stocks.

Consider Vanguard’s Lower-Cost Alternative

The Vanguard FTSE Emerging Markets ETF (NYSEARCA:VWO) offers a simpler approach with a 0.07% expense ratio and $141 billion in assets. That’s nearly four times cheaper than FDEM with far greater liquidity. VWO tracks a broad market-cap-weighted index without factor tilts, meaning more straightforward exposure but potentially higher volatility.

The choice depends on whether you value FDEM’s factor-based risk management enough to justify higher costs and smaller fund size. For most retirees building core emerging markets exposure, VWO’s scale and cost advantage matter more than factor tilts.

FDEM works best as a diversification tool for retirees comfortable with emerging markets volatility and willing to pay for factor-based risk management, but the small asset base and irregular dividends require careful consideration against simpler, cheaper alternatives.