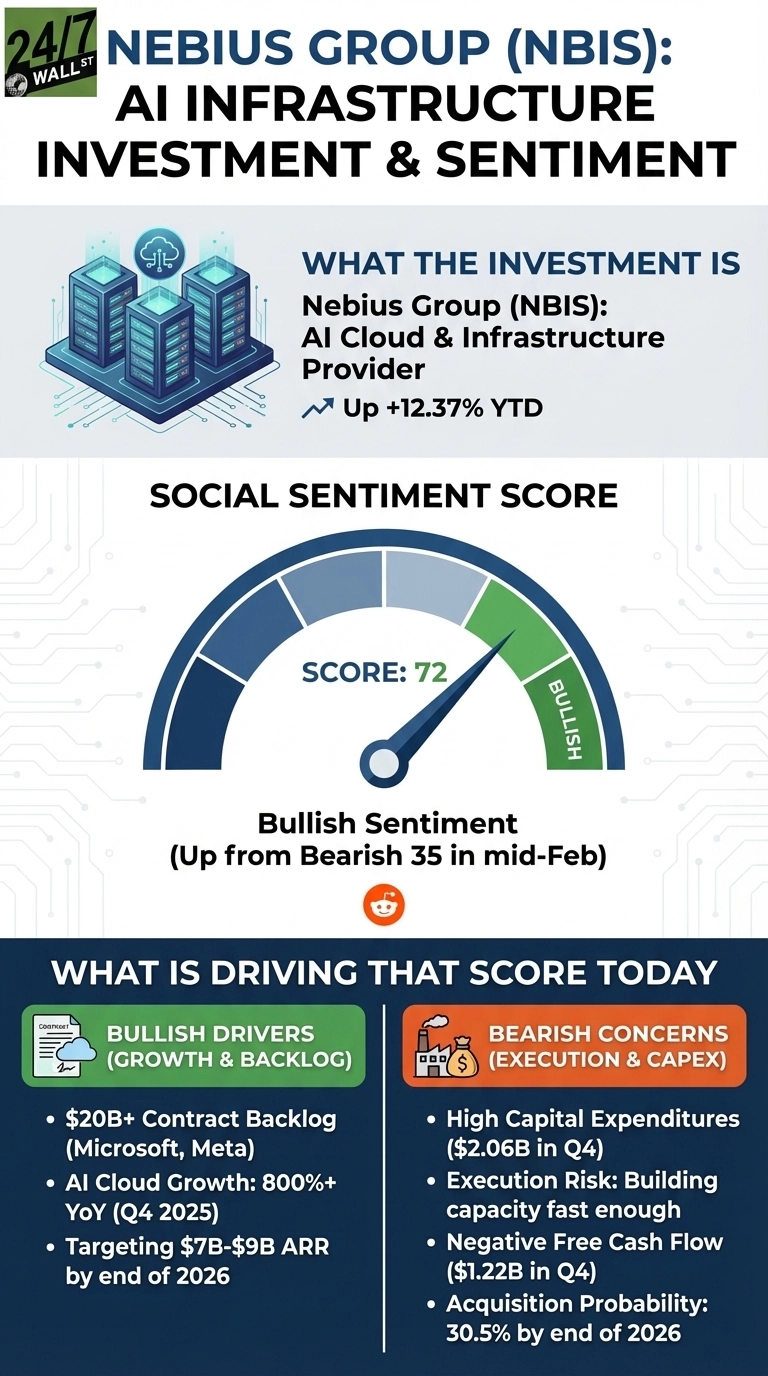

Nebius Group (NASDAQ:NBIS | NBIS Price Prediction) is up 10.5% year-to-date, trading around $93 Monday morning, all while Reddit sentiment has climbed from a bearish 35 in mid-February to a bullish 72 today, driven by a contract backlog that would make most AI startups dizzy. The question retail investors keep circling back to: can Nebius actually build fast enough to collect on them?

The contract wins are real. Nebius has secured a multi-year deal with Microsoft worth up to $19.4 billion and a $3 billion infrastructure agreement with Meta, with a confirmed backlog exceeding $20 billion. The AI Cloud segment grew by more than 400% year-over-year in Q3 2025, reaching sold-out capacity. Management is targeting $7 billion to $9 billion in annualized run-rate revenue by end of 2026, up from $551 million at year-end 2025. That is a roughly 6x jump in twelve months, contingent entirely on execution.

Sentiment Whiplash After Q4

Retail enthusiasm peaked at 95 on February 11-12, the day before earnings. Then you have Q4 revenue of $227.7 million, which missed the $244 million consensus estimate by about 7%, and sentiment dropped to 35 by February 15. The miss was supply-driven, not demand-driven. Capacity was sold out. That distinction matters, but it did not stop the selloff.

The bull case on r/wallstreetbets was captured in a pre-earnings post that garnered 280 upvotes:

NBIS full port leaps

by u/Charming-Priority859 in wallstreetbets

“This is the most asymmetrical AI play on the market rn,” wrote Charming-Priority859, pointing to Nebius’s vertical integration and the fact that “the core business is less than the $19B deal with Microsoft and $3B deal with Meta combined.”

Bears are not arguing demand, and they are arguing about capital structure. Nebius spent $2.06 billion on capex in Q4 alone and is planning $16 billion to $20 billion in total capex for 2026 across nine new data center sites. Free cash flow was negative $1.23 billion in Q4, and total liabilities have grown to $7.84 billion. An ATM equity program authorizing up to 25 million new shares adds dilution risk on top of the debt load.

The Hyperscaler Context

Amazon (NASDAQ:AMZN)’s AWS grew 24% YoY, and Amazon is planning ~$200B in CapEx in 2026. Alphabet (NASDAQ:GOOGL)’s Google Cloud grew 48% YoY with an annual run rate above $70 billion. Both hyperscalers are capacity-constrained, which is precisely why a customer like Microsoft would sign a $19 billion deal with Nebius rather than wait. This leads to one answer: the tailwind is real. The execution gap between signing contracts and connecting gigawatts of power is where the risk lives.

Prediction markets are pricing in a 30.5% probability that Nebius gets acquired before the end of 2026, higher than OpenAI at 8.7% or Anthropic at 13%. Analysts note that key milestones to watch include connected power capacity and whether the 2026 ARR trajectory stays on pace for the $7-9 billion target.