Walmart (NASDAQ:WMT | WMT Price Prediction) and Costco (NASDAQ:COST) both posted strong quarterly results, though their dividend growth rates differ sharply. Walmart is a Dividend King with 52-plus consecutive years of increases. Costco is growing its regular payout at more than twice Walmart’s recent rate.

Omnichannel Momentum vs. Membership Machine

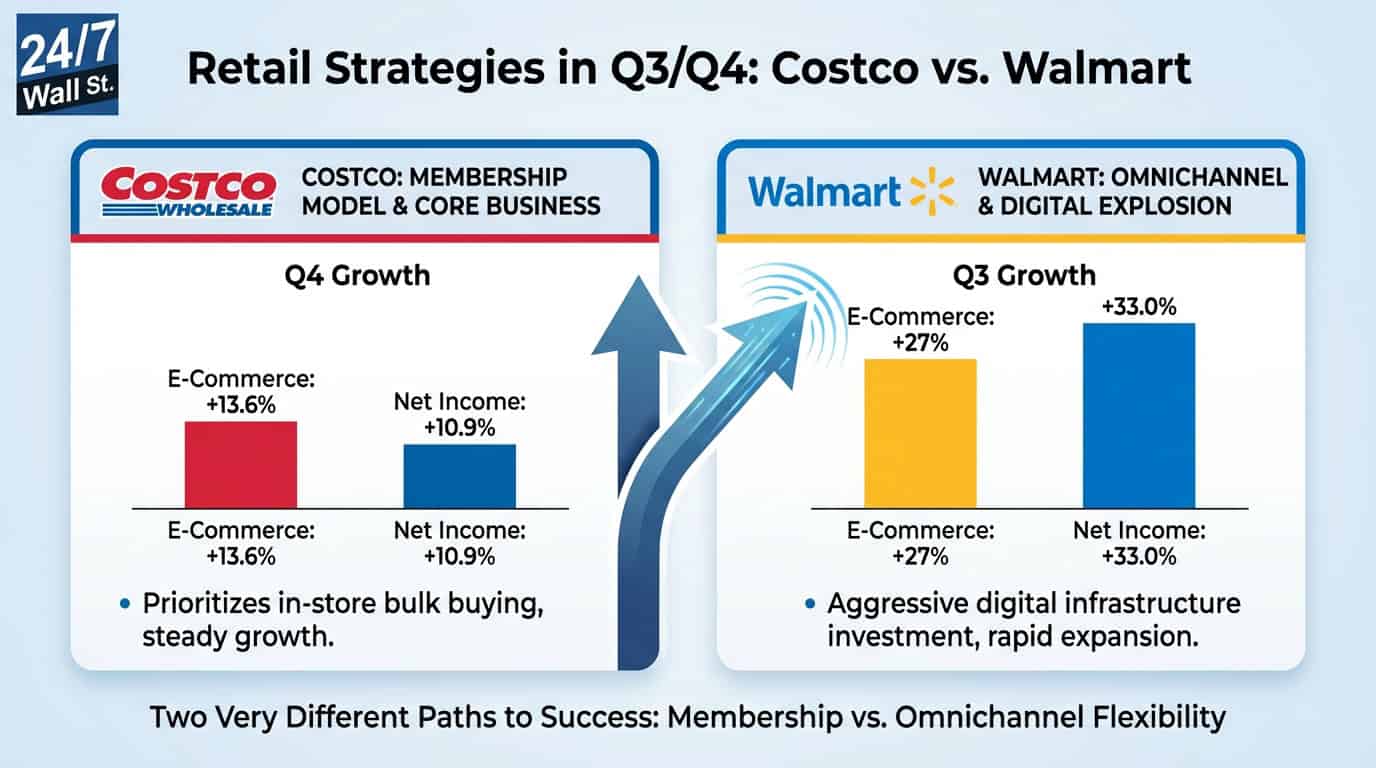

Walmart’s Q4 FY26 results showed a business firing across nearly every channel. Walmart U.S. comparable sales rose 4.6%, while global eCommerce grew 24% year over year and now represents 23% of Walmart U.S. net sales, a record. The advertising business reached roughly $6.40 billion annually, growing 37% including VIZIO.

Costco’s Q2 FY26 told a different story. Comparable sales rose 7.4%, and the membership engine kept humming. Paid memberships reached 82.1 million, with a worldwide renewal rate of 89.7%. Membership fee income grew 13.6% to $1.355 billion.

Digital momentum accelerated with digitally-enabled comparable sales up 22.6% and app visits surging 63%. Costco’s model is intentionally lean: gross margin runs at roughly 3.67% operating margin, with profitability flowing from volume and member loyalty rather than product markup.

| Business Driver | Walmart | Costco |

|---|---|---|

| Comp Sales Growth | +4.6% (U.S.) | +7.4% (global) |

| eCommerce Growth | +27% (U.S.) | +22.6% (digitally-enabled) |

| Key Revenue Lever | Advertising + omnichannel | Membership fees + Kirkland |

| Gross Margin | 24.0% | 11.02% |

The Dividend Gap Is Widening

Walmart raised its annual dividend to $0.99 per share for 2026, up from $0.94 in 2025. The quarterly increase from $0.235 to $0.2475 represents roughly 5.3% growth.

Costco’s regular quarterly dividend moved from $1.16 to $1.30, effective in early 2026, an increase of approximately 12% (more than twice Walmart’s pace).

Annualized, Costco’s regular dividend now runs at $5.20 per share. Add Costco’s history of special dividends, including a $15 special dividend paid in December 2023, and total shareholder returns diverge from yield alone.

| Dividend Metric | Walmart | Costco |

|---|---|---|

| Current Annual Regular Dividend | $0.99 | $5.20 |

| Recent Dividend Growth Rate | ~5.3% | ~12% |

| Dividend Yield | 0.73% | 0.5% |

| Special Dividends | None recent | Yes, most recently $15.00 in 2023 |

What to Watch Next

Walmart guided for FY27 net sales growth of 3.5%-4.5% and adjusted EPS of $2.75-$2.85. Tariff exposure and rising capex of $26.64 billion in FY26 are headwinds. Watch whether the advertising business continues scaling and whether Walmart+ membership revenue, up 15.1% globally, keeps compounding.

Costco is targeting roughly 28 net new warehouses in FY2026, reaching 942 total warehouses. With $17.38 billion in cash on hand and free cash flow of $7.84 billion, the balance sheet supports expansion. Monitor whether membership renewal rates hold above 89% as new warehouses open in less-proven markets.

Why Costco Edges Out for Dividend Growth Investors

Walmart’s streak is impressive, and at a 41.15% one-year price gain, total return has been strong. But the dividend itself is growing slowly relative to valuation. Costco’s regular dividend compounds faster, and the company has shown willingness to return surplus cash through special payouts when the balance sheet allows.

Walmart fits if you prioritize consistency and mass-market retail dominance. Costco makes the stronger case for long-term income growth, pairing faster dividend increases with a membership model that generates deeply loyal, recurring revenue. Neither is cheap at current multiples, so entry price matters for both.