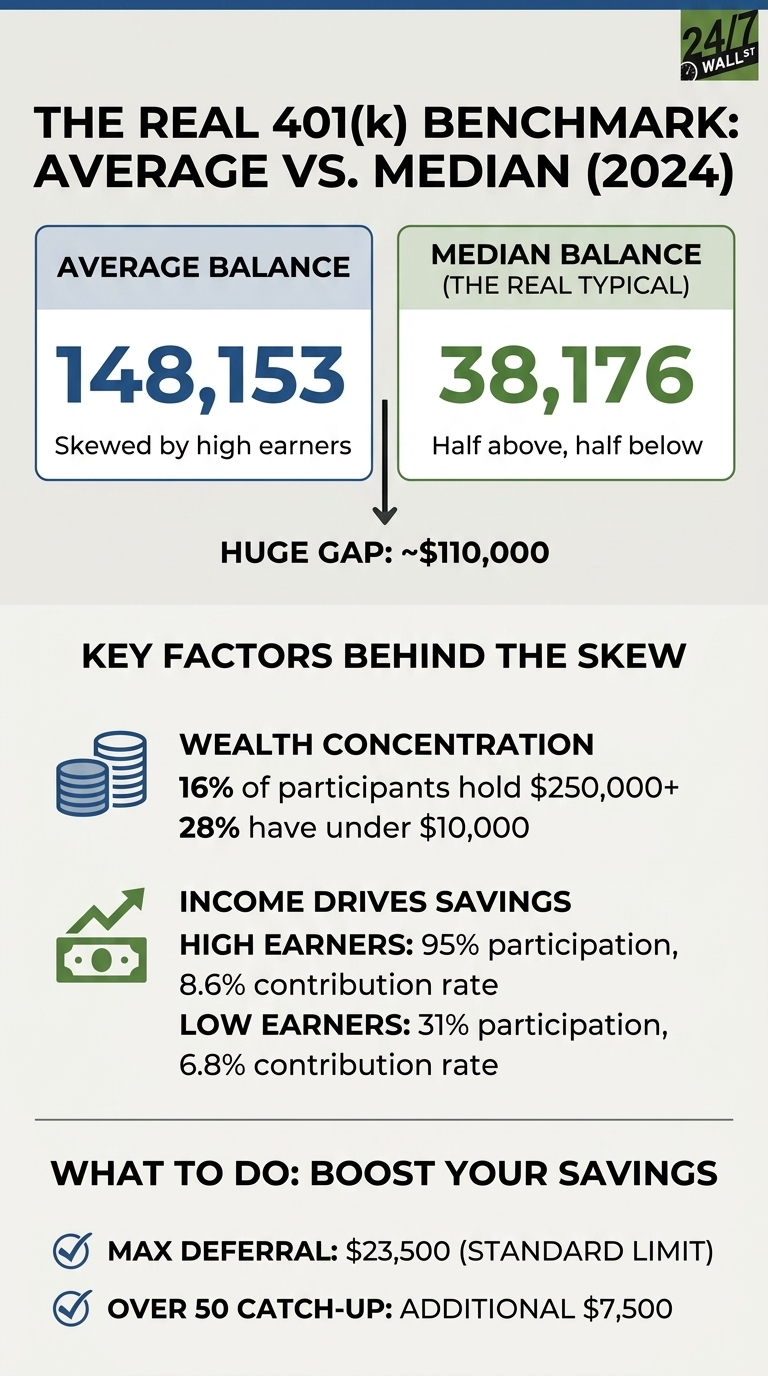

The headline number from Vanguard’s 2025 How America Saves report looks reassuring at first glance: the average 401(k) account balance reached $148,153 in 2024. That figure suggests the typical American worker is sitting on a six-figure retirement nest egg. The median tells a different story. The median balance, the one that actually describes the worker in the middle of the distribution, was $38,176. The roughly $110,000 gap between those two numbers reflects the distribution of balances.

Why the Average Distorts

A simple illustration explains the distortion. If 10 people each have $5,000 saved and one person walks in with $5 million, the median balance is still $5,000. The average jumps to roughly $459,000. Nothing changed for the typical saver, but the headline number now suggests everyone is wealthy.

The same dynamic plays out in 401(k) data. Vanguard explicitly notes that the median “represents the typical participant: Half of all participants had balances above the median, and half had balances below.” The average, by contrast, “is indicative of participants at about the 75th percentile”, meaning roughly 75% of workers have balances below it.

Where the Skew Comes From

The Macro Backdrop Makes the Gap Worse

The report shows that the savings environment isn’t just about income; it’s about how long people stay in the game and how often they tap their funds. While the average account balance is high, tenure is a massive divider. Participants with more than 10 years in their plan have an average balance of $324,510, while those with less than two years have a median of just $6,140.

The pressure isn’t just coming from inflation, but from plan leakages. In 2024, 12% of participants had an outstanding plan loan. Furthermore, while the market was strong, hardship withdrawals rose to 4.8%, with 35% of those participants citing the need to prevent foreclosure or eviction. This suggests that for many “middle-of-the-pack” savers, the 401(k) is increasingly doubling as an emergency fund.

Reading the Real Number

For a savvy reader, the median of $38,176 is the most honest benchmark for the “typical” American worker. The report makes it clear that the $148,153 average is a “75th percentile” number, meaning if you have that much, you are already doing better than three-quarters of all other savers.

The real drivers of the balance gap are simple but hard to beat: time and consistency. The report shows that the small group of savers driving the average higher is made up of those who have stayed with the same employer for over a decade and have reached the “Gold Standard” total contribution rate of 15%.

Reference Points

- Vanguard and the Federal Reserve Survey of Consumer Finances publish age-bracket median 401(k) balances, which sit closer to the typical participant than headline averages.

- The 8.6% contribution rate at the top income tier compared with 6.8% at the bottom is one driver of the long-run balance gap.

- The standard 401(k) deferral limit is $23,500, with an additional $7,500 catch-up available for workers over 50.