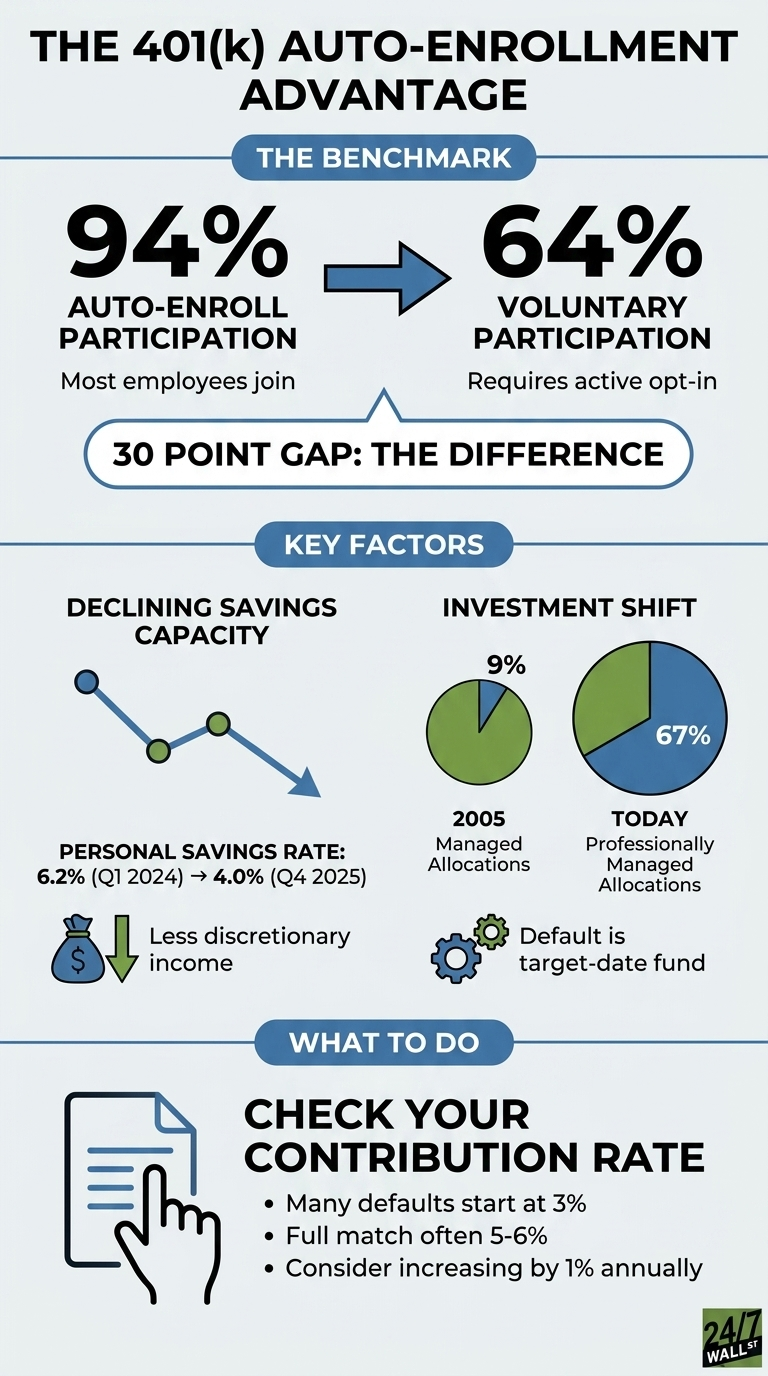

The single biggest design lever for American retirement savings is whether a plan automatically enrolls new hires. According to Vanguard’s 2025 How America Saves report, plans that automatically enroll achieve a 94% participation rate, while plans that require workers to opt in see just 64% sign up. That 30-percentage-point spread is the difference between a workforce that saves and one that does not.

Why The Default Setting Matters Now

The plan data makes the design choice more consequential than it was a decade ago. Hardship withdrawals hit 4.8% of participants in 2024, up from 3.6% in 2023, with 35% of those withdrawals going to avoid foreclosure or eviction. Meanwhile, 13% of participants carried an outstanding loan, and the average loan amount was about $11,000. When workers are already tapping into retirement accounts for emergencies, voluntary contributions to future savings become the easiest line item to skip. A default contribution removes that decision entirely.

The 30 Point Gap, In Plain Terms

The Vanguard data describes two parallel workforces inside the same economy. In the auto-enrollment world, almost everyone is in the plan. In the voluntary world, roughly a third of eligible employees are not participating at all, and therefore not capturing employer match dollars they have already earned through their labor.

The contrast is sharper among workers with less than two years of tenure. Auto-enrolled employees in that group participate at a 90% rate compared with 40% for voluntary plans. Their average total contribution rate is 12.1%, up from 7.6%. A 22-year-old who joins an auto-enrollment employer is contributing at roughly twice the rate of an identical 22-year-old at a voluntary plan, before either of them has thought about retirement at all.

The Quiet Investment Shift Behind The Numbers

The default design has reshaped how the money is invested, not only whether it gets saved. 67% of Vanguard participants now hold professionally managed allocations, primarily target-date funds, up from just 9% in 2005. 59% hold a single target-date fund, which automatically adjusts equity exposure as the worker ages.

Concerns about workers cashing out when they change jobs have also moderated. Vanguard reports that 97% of plan assets available for distribution are preserved for retirement, and 83% of terminated participants continue to preserve their assets.

Implications For Young Professionals

For workers in the first five years of their career, the data points to three areas of focus:

- The plan’s default contribution rate. One-third of auto-enrollment plans still start workers at 3%, which captures participation but often leaves employer match dollars unclaimed. The average employee must defer 6.5% of pay to capture the full match; the median is 6.0%.

- The default investment. Nearly all automatic enrollment plans now default to a target-date or balanced fund, with 98% specifically choosing a target-date fund. Only 1% use a money market or stable value default. The 67% of Vanguard participants in professionally managed allocations reflects a design that assumes long-dated equity exposure for younger workers.

- Automatic escalation, where offered. Two-thirds of automatic enrollment plans default to a 1% annual increase, though caps vary. Thirty-nine percent of plans cap the increase at 10%, while 37% set caps between 11% and 20%. These features close the gap between the typical starting contribution rate and the levels most retirement calculators reference.

The labor market gives most workers room to act. The unemployment rate stood at 4.3% in March 2026, within the range typically associated with broad access to employer-sponsored benefits. The HR choice has already been made at many companies. The remaining choice is the employee’s.