The image of the retail day trader hunched over four monitors, scalping options between Slack messages, has dominated financial media since the meme stock era. The reality inside the average 401(k) plan looks nothing like that. According to Vanguard’s 2025 How America Saves report, only 5% of nonadvised participants made any portfolio exchanges in 2024, down from 20% in 2004. Among investors who hold a single target-date fund, the figure drops further: just 1% traded at all. The default setting for retirement investing has quietly become inertia, and the data suggests that may be working in savers’ favor.

The Benchmark: 5% Traded, 95% Did Nothing

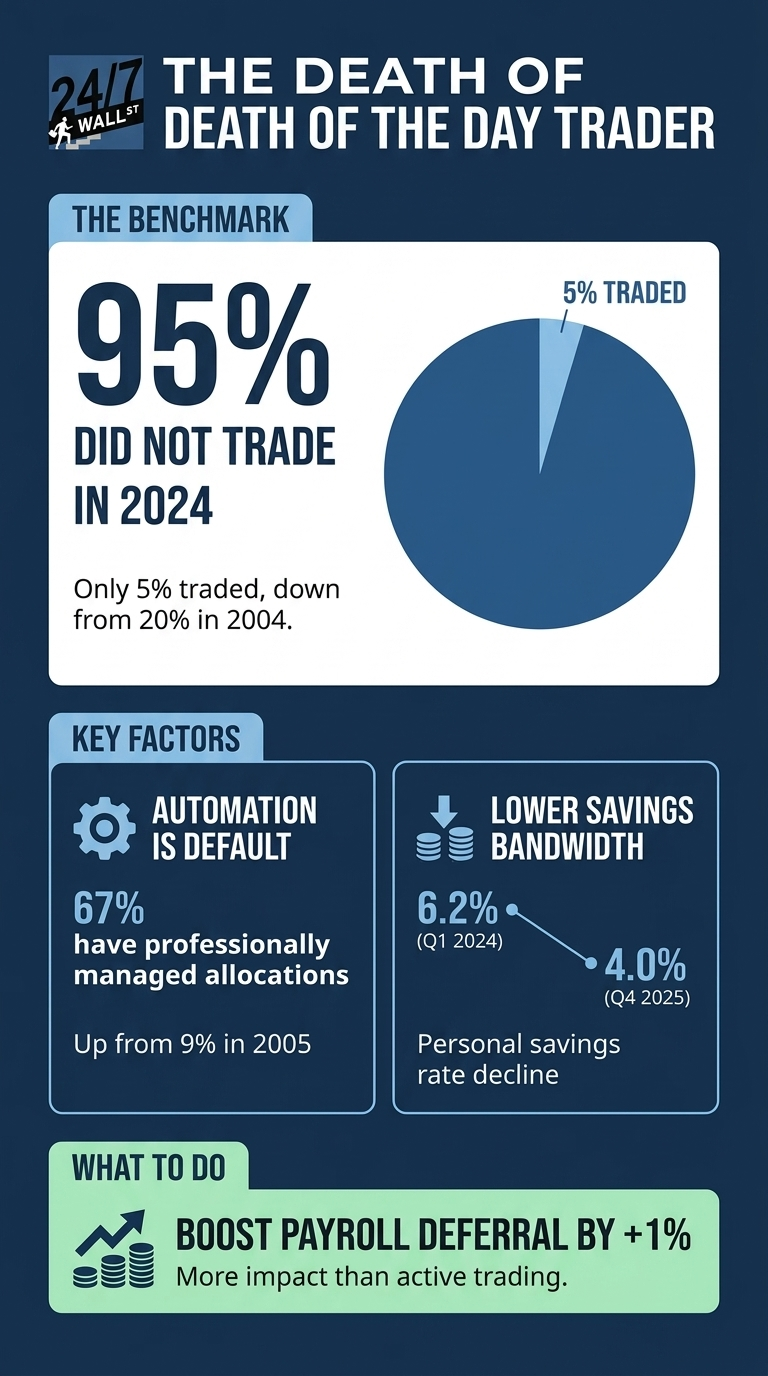

The headline number from Vanguard’s review of millions of defined contribution accounts is the trading rate. 5% of participants without an advisor exchanged any portion of their portfolio in 2024. That rate has fallen by three-quarters over two decades. The cause is structural.

Sixty-seven percent of Vanguard participants now hold professionally managed allocations, meaning a target-date fund, a balanced fund, or a managed account does the rebalancing for them. That figure was 9% in 2005. Within that group, 59% are pure target-date fund investors, holding one fund and nothing else. Of plans that offer target-date funds, 84% of participants use them, and 64% of new contributions in 2024 flowed into these vehicles, up from 46% in 2015.

Why Doing Nothing Has Paid

The macro backdrop frames why passivity has been rewarded. The Vanguard Total Stock Market ETF (NYSEARCA:VTI | VTI Price Prediction), a reasonable proxy for what a hands-off saver in a US equity fund captured, returned 30.26% over the past year and 234.12% over the past ten years. That return came through real volatility. The CBOE Volatility Index spiked to 31.05 on March 27, 2026 before falling back to 18.71 by April 24. Active traders reacting to that spike would have sold into fear; participants in target-date funds did not see the spike on their statements because they did not look.

Consumer sentiment also helps explain the behavior. The University of Michigan index sat at 53.3 in March 2026, in recessionary territory, with a 12-month range of 51.0 to 61.7. The personal savings rate has compressed from 6.2% in Q1 2024 to 4.0% in Q4 2025. Households juggling tighter cash flow and persistent pessimism appear to have less appetite, and less b

andwidth, for active portfolio decisions.

What Changed Between 2004 and 2024

Three forces converged to produce the shift:

- Automatic enrollment. Plans default new hires into a target-date fund matched to their expected retirement year. The participant never makes a fund selection.

- Qualified default investment alternative status. Regulatory cover encouraged plan sponsors to use target-date funds as the default, accelerating the move from money market funds and stable value as defaults.

- Auto-rebalancing inside the fund. A target-date fund rebalances on its own schedule, so the participant does not need to log in to maintain an allocation.

The result: among the 5% of participants who did trade in 2024, the most common action was rebalancing rather than market timing. The day trader archetype is essentially absent from workplace retirement data.

Is Extreme Passivity a Win?

For most savers, the evidence points one direction. Decades of academic work show retail market timing tends to subtract returns. A diversified equity allocation held through the -0.6% Q1 2025 GDP contraction and the subsequent 4.4% Q3 2025 print outperformed most attempts to trade the swings. The cost is that target-date glide paths are generic. A 45-year-old with a paid-off house and a public pension is not the same investor as a 45-year-old with a mortgage and no other savings, but both may end up in the same 2045 fund.

Considerations for Plan Participants

- Default vintage alignment. Plans sometimes default contributions into a target-date fund whose retirement year does not match the participant’s expected timeline, an item often surfaced during a routine plan review.

- Contribution rate sensitivity. With the savings rate at 4.0%, research has generally found that a one percentage point payroll deferral increase has a larger effect on long-term outcomes than trading activity.

- Expense ratio dispersion. Target-date fund fees vary widely across plans, and a fund held passively can still carry an expense ratio that materially compounds over decades.