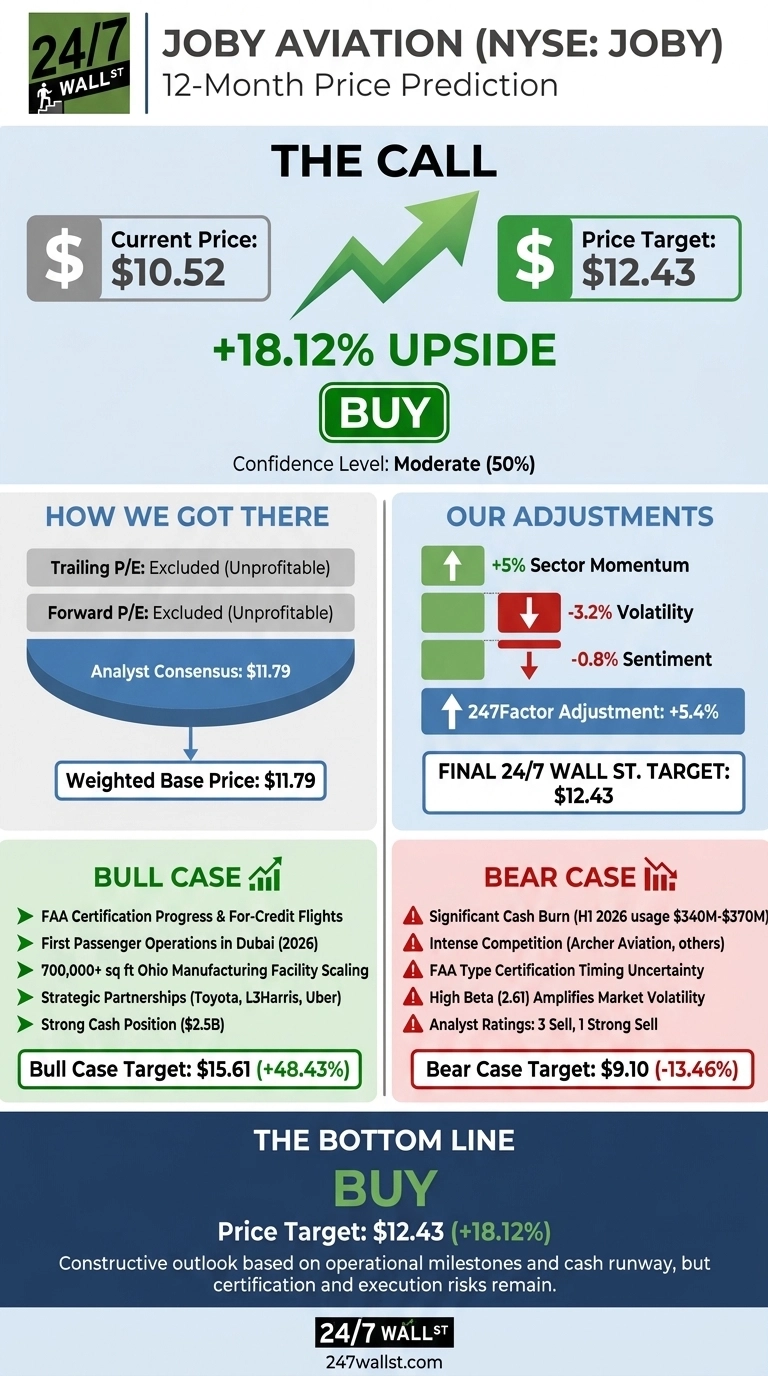

The 24/7 Wall St. price target for Joby Aviation (NYSE:JOBY | JOBY Price Prediction) is $12.43, which implies 18.12% upside from the current $10.52 share price. Our proprietary model rates Joby a buy with moderate (50%) confidence, reflecting genuine certification momentum balanced against heavy cash burn and a 2.61 beta that amplifies every macro headline.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $10.52 |

| 24/7 Wall St. Price Target | $12.43 |

| Upside | 18.12% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Volatile Year That Just Found a Floor

Joby has been a rollercoaster. Shares are up 65.41% over the past year and 20.92% in the last week, but down 20.3% year to date after sliding from a January high. The stock now sits well below its 52-week high of $20.95 and comfortably above the 52-week low of $6.42.

The first quarter earnings report provided the catalyst for the recent bounce. Joby reported $24 million in revenue (beating a $20.2 million consensus), a $110 million net loss, and most importantly $2.5 billion in cash, cash equivalents and short-term investments after the February capital raise. Management also confirmed eIPP program selections across up to 11 states and the first flight of FAA-conforming aircraft N547JX for Type Inspection Authorization testing.

Why Bulls See a Breakout Ahead

The bull case rests on certification crossing the finish line. Q4 2025 produced a record 18-point FAA Stage 4 progress increase, and the SR3 audit is now complete. Management guides 2026 revenue of $105 million to $115 million, with first paid passengers in Dubai this year.

Add the 700,000+ square foot Dayton, Ohio facility targeting up to 500 aircraft per year, an up to $250 million letter of intent in Kazakhstan, the L3Harris defense partnership, and Toyota investment, and the long-term opportunity is real. Our bull-case 12-month target is $15.61, a 48.43% return.

The Risks Worth Watching

Cash burn is the bear case in one number: management guided $340 million to $370 million of usage in H1 2026 alone. FY2025 operating cash flow was -$509.89 million, and competition from Archer is fierce.

Bears would also note 3 sell ratings and 1 strong sell against just 2 buys. Counterfactually, the $929.84 million FY2025 net loss is heavily distorted by non-cash warrant revaluations, and the $2.5 billion cash balance funds operations well into FAA certification. Still, the bear-case 12-month target is $9.10.

Canaccord analyst Austin Moeller lowered the firm’s price target on Joby Aviation to $11.50 from $15.50 and keeps a Hold rating on the shares.

Our Take: Constructive, With Caveats

Our price target of $12.43 and buy rating reflect a stock that has already absorbed a painful drawdown while operational milestones keep arriving. The setup looks constructive for investors who can stomach the 2.61 beta and want exposure to a leading eVTOL platform with $2.5 billion of runway. The thesis weakens if FAA Type Certification slips into 2027 or if Dubai commercial launches face delays. Confidence is moderate, and the path will be choppy.

Looking further ahead, here is where our model projects Joby could trade in the coming years, anchored to our 5-year base case and scaled to interim milestones.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $12.43 |

| 2027 | $13.75 |

| 2028 | $15.10 |

| 2029 | $16.40 |

| 2030 | $17.72 |

These projections assume Joby achieves FAA Type Certification, scales the Ohio facility on schedule, and converts its Dubai, Saudi, and U.S. eIPP commitments into recurring revenue. Significant upside or downside could result from certification timing, dilution from future capital raises, or competitive displacement by Archer and other eVTOL entrants.