Jim Cramer made a call on Mad Money that deserves a closer look. A viewer asked about Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction), and Cramer described it as a “rule of 40 juggernaut” before delivering his view:

“Palantir is basically building a new base because boy, their business is strong. I’m relying on the customers. The customers love them. And therefore I think they’ve got a great product. And therefore I think they will have a great 2026 and 2027.”

— Jim Cramer, Mad Money

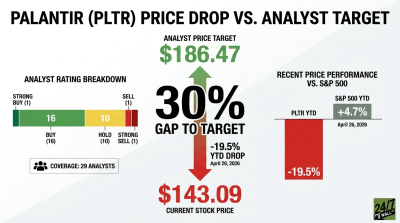

Since I’ve been following Palantir, and the tension between its fundamentals and its valuation has never been more obvious. The stock is sitting at $146.49, down 17% year-to-date after hitting a 52-week high of $207.52.

Look, the stock got overheated and sellers came out, but it’s clear the business fundamentals remain strong. The numbers back that up.

The Business Is Accelerating, Not Slowing

Palantir’s Q4 2025 results, filed February 2, 2026, showed revenue of $1.406 billion, up 70% year-over-year, with adjusted EPS of $0.25 against a $0.18 consensus estimate. U.S. commercial posted $507 million in revenue, up 137% year-over-year, a growth rate that accelerated every single quarter in 2025, from 71% in Q1 to 93% in Q2 to 121% in Q3 to 137% in Q4.

The Rule of 40 score hit 127% in Q4. Most software companies celebrate cracking 40%. CEO Alex Karp said in the SEC earnings release:

“We are an n of 1, and these numbers prove it. Palantir is alone in choosing to exclusively focus on scaling the operational leverage made possible by the rapid advancements of AI models, a trend that we first called ‘commodity cognition’ well before others started repeating it.”

— Alex Karp, CEO, Q4 2025 Earnings Release

For 2026, management guided revenue of $7.182–$7.198 billion, implying 61% growth, with U.S. commercial revenue expected to exceed $3.144 billion. That’s the foundation behind Cramer’s “great 2026 and 2027” call.

The Valuation Question You Can’t Ignore

The stock trades at a trailing P/E of roughly 233x and a forward P/E of 114x. Analysts carry a consensus target of $186.60, with 16 buy ratings, 10 holds, and 2 sells. Insider activity has been net selling, with $140.54 million in insider sales over the past three months noted in recent filings.

Recent partnerships with Stellantis, extending the Foundry platform relationship for five years, and adoption in healthcare and financial services, show the AIP platform is landing real enterprise customers. The contracts are growing and revenue visibility is strong.

If you believe AI-driven enterprise software adoption is still early, Palantir’s accelerating commercial growth and $2.270 billion in free cash flow generated in FY 2025 make a case for patience. If the valuation keeps you up at night, that’s legitimate too. What I’m watching next is Q1 2026 results against the $1.532–$1.536 billion revenue guidance. That print will tell us whether the acceleration is holding and whether Cramer’s base-building thesis holds. Cramer opened by calling Palantir a rule of 40 juggernaut building a base.

The open question has always been whether the valuation can grow into itself. At 127% Rule of 40, accelerating U.S. commercial growth, and $2.270 billion in free cash flow, the business is doing its part. The stock’s next move depends on whether the numbers keep pace with the story.