I keep buying Palantir (NASDAQ:PLTR | PLTR Price Prediction), and the 20.57% drawdown year to date has only made my finger heavier on the buy button. This is the confession part: I am accumulating a stake in the one software company I believe is turning generative AI into operating leverage at industrial scale, and every pullback in 2026 has looked like a gift to someone with a long horizon.

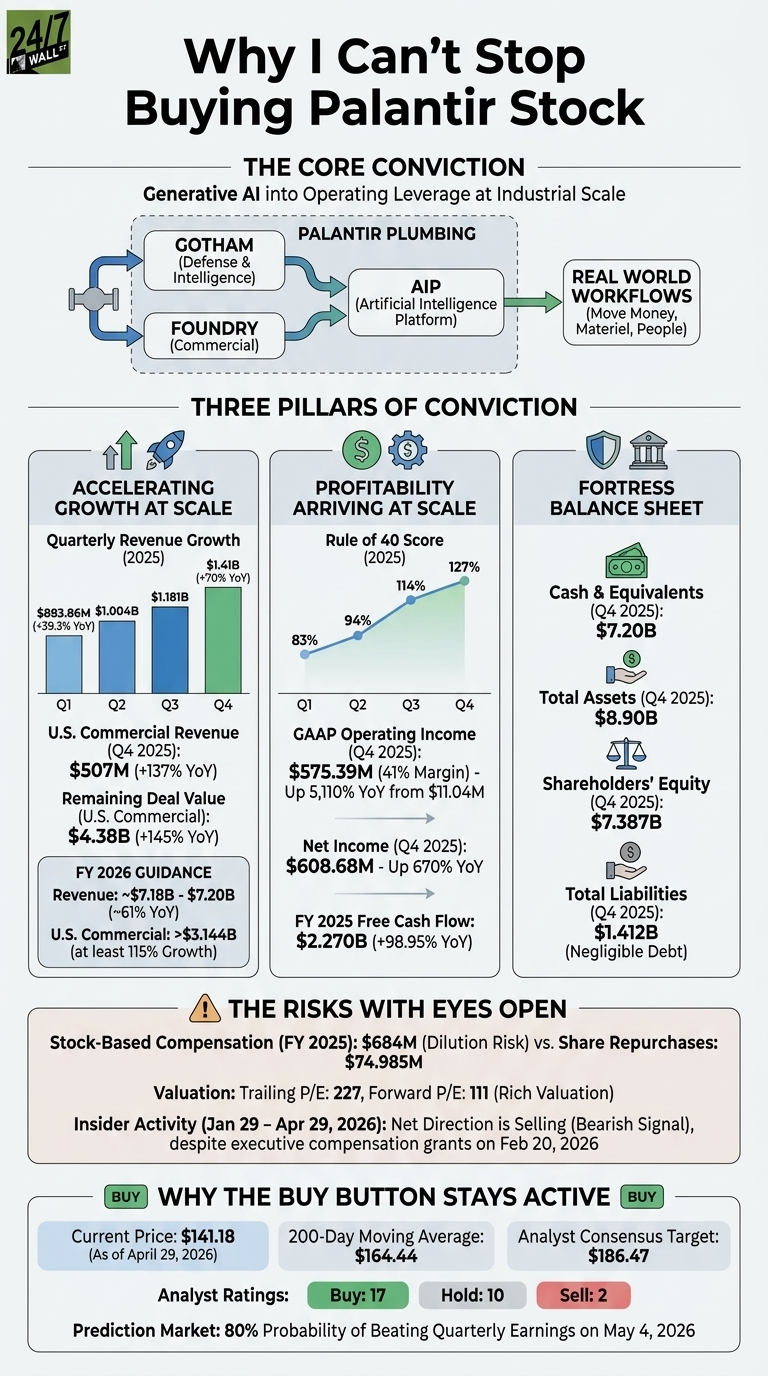

The thesis is simple in plain English. Palantir sells the plumbing that lets large enterprises and governments wire AI directly into the decisions that run their business. Gotham handles the defense and intelligence side. Foundry runs the commercial side.

AIP, the Artificial Intelligence Platform, is the layer that takes the models everyone is hyping and turns them into workflows that move money, materiel, and people. CEO Alex Karp calls this “commodity cognition”, and the financials say customers are paying real cash for it.

Three Reasons The Conviction Holds

The first reason is growth that is accelerating at scale. Quarterly revenue stepped from $883.86 million in Q1 2025 (up 39.3% YoY) to $1.004 billion in Q2, then $1.181 billion in Q3, and finally $1.41 billion in Q4 2025, up 70% year over year.

U.S. commercial, the part of the business most exposed to AIP demand, grew 137% in Q4 to $507 million, with remaining deal value of $4.38 billion, up 145% YoY. That is forward visibility I can underwrite. Management is now guiding FY 2026 revenue of $7.18 billion to $7.19 billion, roughly 61% YoY growth, with U.S. commercial expected to grow at least 115%.

The second reason is profitability arriving at scale. Q4 GAAP operating income was $575.39 million at a 41% margin, up 5,110.49% YoY from $11.04 million. Net income reached $608.68 million, up 670.39%. Full-year free cash flow hit $2.270 billion, up 98.95%.

The Rule of 40 score, which combines growth and free cash flow margin, climbed from 83% in Q1 to 127% by Q4. I have followed software for years and I rarely see that combination.

The third reason is the balance sheet. Palantir ended Q4 with $7.20 billion in cash and equivalents, total assets of $8.90 billion, shareholders’ equity of $7.38 billion, and total liabilities of just $1.41 billion. That is a war chest, with negligible debt and ample funding.

The Risk I Own With Eyes Open

I own the risks with eyes open. The honest risk is twofold. Stock-based compensation ran $684 million for FY 2025, against share repurchases of only $74.98 million, which means I am being diluted while the company prints cash. Layered on top, the valuation is rich: a trailing P/E of 227 and a forward P/E of 111 leave zero room for a stumble.

My answer is that the operating leverage thesis already absorbs that dilution. With FY 2026 adjusted free cash flow guided to $3.92 billion to $4.12 billion, the cash generation can outrun the share count if growth holds. That is the bet I am willing to make.

Why The Buy Button Stays Active

The shares trade at $141.18, below the 200-day moving average of $164.44, while Wall Street’s consensus target sits at $186.47 with 17 buy ratings against 10 holds. Polymarket’s crowd assigns an 80% probability that Palantir beats its next quarterly earnings on May 4. Insider compensation grants on February 20, 2026 showed the senior team, including Karp, Sankar, and Cohen, taking large equity positions in the business they run.

I keep buying Palantir because the company is doing the rarest thing in software: growing faster, earning more, and generating more cash at the same time, and the market keeps offering me the stock at a discount to its own recent highs. I will keep adding until that stops being true.